Innovative Energy Technologies in Austria: Market Development 2020

Bibliographic Data

18/2021P. Biermayr, C. Dißauer, M. Eberl, M. Enigl, H. Fechner, B. Fürnsinn, M. Jaksch-Fliegenschnee, K. Leonhartsberger, S. Moidl, E. Prem, C. Schmidl, C. Strasser, W. Weiss, M. Wittmann, P. Wonisch, E. Wopienka

Publisher: BMK

German, 273 pages

Content Description

Motivation, method and content

The documentation and market research in the field of technologies for the use of renewable energy sources creates a basis for the planning and decision making in politics, economy, research and development. The aim of this market study "Innovative energy technologies in Austria – market development 2020" is to lay a foundation in the following fields: biomass, photovoltaics, solar thermal collectors, heat pumps and wind power.

Methods used are: questionnaires handed out to manufacturers, trading firms and installation companies as well as questionnaires for funding providers at the national and local governments. Furthermore information is gathered with a survey of literature, the evaluation of available statistics and internet research. The obtained data is displayed in time series to provide the starting point for deeper analysis and strategical considerations.

First the market development is illustrated by production numbers or installed capacities and then the energy gain is calculated taking into account the life cycle of the machinery. The necessary support energy for the main and auxiliary machinery is discussed and savings in gross and net of greenhouse gas emissions are calculated. The graphically displayed turnovers and the job creating effects eventually show the impact of the various technologies in Austria. Results are shown in alphabetical order of technologies.

Introduction

The influencing factors of the market diffusion of the renewables were widespread in 2020. The consequences of the Corona crisis remained widely manageable in 2020 – as was generally the case in the building sector and classical factors as the price of fossil energy, the existing energy-political framework and the competition among the technologies for the use of renewable energy dominated the events. Against this background an increase of the domestic market in the areas biomass boilers, photovoltaics and heat pumps could be recorded while clear declines had to be registered in the areas biomass stoves, solar thermics and wind power.

The inhomogenous market development of the last years was thus also continued in 2020. In the last decade in Austria a significant and stable growth of annually newly installed capacities could only be observed in the area of heat pumps whereas lately in the areas biomass boilers and photovoltaics there could also be observed a market growth lasting some years. However the current market development is not at all sufficient for reaching the national energy and climate targets for 2030 or 2040. The set goals can only be reached by an immediate, comprehensive and ambitious implementation of effective and efficient energy and ecopolitical instruments whereas the increase of the market diffusion of all technologies for the use of renewable energy has to go along with an increase of energy efficiency in all useful energy sectors.

Solid biomass - fuels

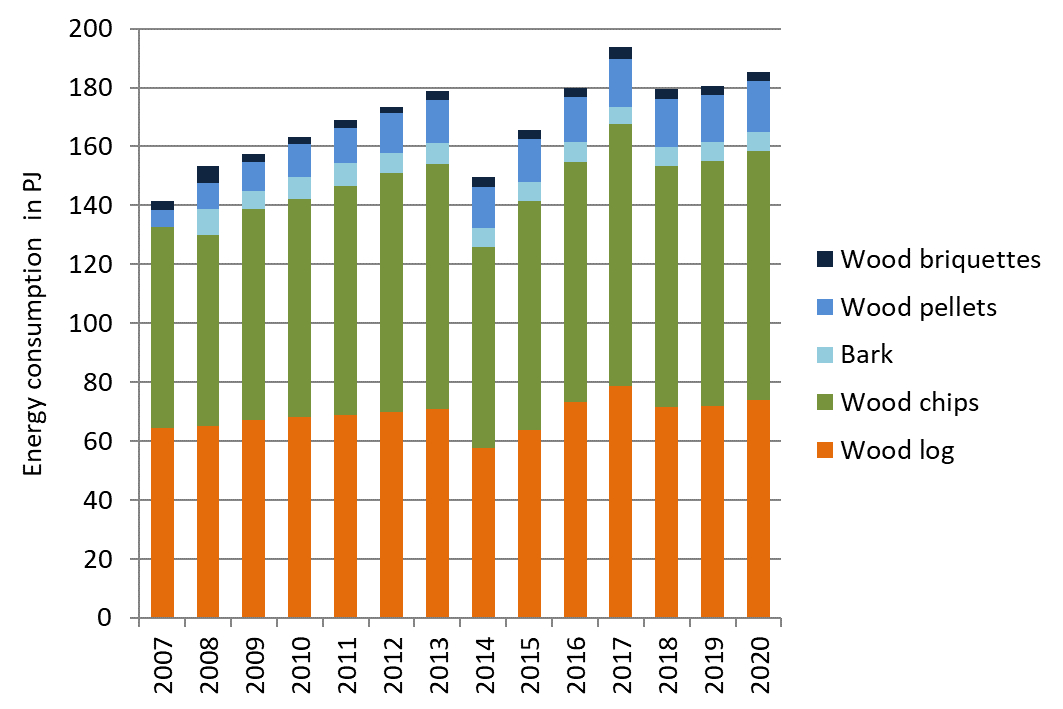

The energetic utilization of solid biomass has a long tradition in Austria and is still a very important factor within the renewable energy sector. The consumption of final energy from solid biofuels increased from 142 PJ in 2007 to 179 PJ in 2013. In 2014 the consumption of solid biofuels decreased to 150 PJ due to relatively high average temperatures see Figure 7. In the following years the consumption of solid biofuels increased again, in 2017 up to 193.6 PJ. However, due to high temperatures the consumption of solid biofuels decreased to 179.4 PJ in 2018 and to 180.5 PJ in 2019. In 2020 the consumption of solid biofuels increased to 185.25 PJ due to low temperatures and increased sales of biomass technologies. The consumption of wood chips has been increasing since the beginning of the 1980s. In 2020 the wood chips consumption was 84.5 PJ and thus exceeded the consumption of wood logs with 74.0 PJ. The very well documented wood pellet market developed with an annual growth rate between 30 % and 40 % until 2006. This development was then stopped 2006 due to a supply shortage which resulted in a substantive price rise. The market recovered and the production capacity of 28 Austrian pellet manufacturers has been extended to 1.75 million tons a year. In 2020 the national pellet consumption amounts to 17.3 PJ (1,015,000 t).

Fuels from solid biomass contributed to a CO2 reduction of about 9.2 million tons in 2020. The whole sector of solid biofuels made a total turnover of 1.580 billion Euros thus creating 18,376 jobs.

The success of bioenergy highly depends on the availability of suitable biomasses in sufficient volumes and at competitive prices. The availability of biomass feedstock is currently very good. In addition to the traditional use of biomass in the heating sector, the importance of bioenergy as part of a sustainable energy system in combination with other renewables is increasing: biomass fuels are weather-independent energy suppliers. In this context the co-production of electricity and/or material products such as biochar is of great interest in order to ensure the most efficient use of resources.

Solid biomass – boilers and stoves

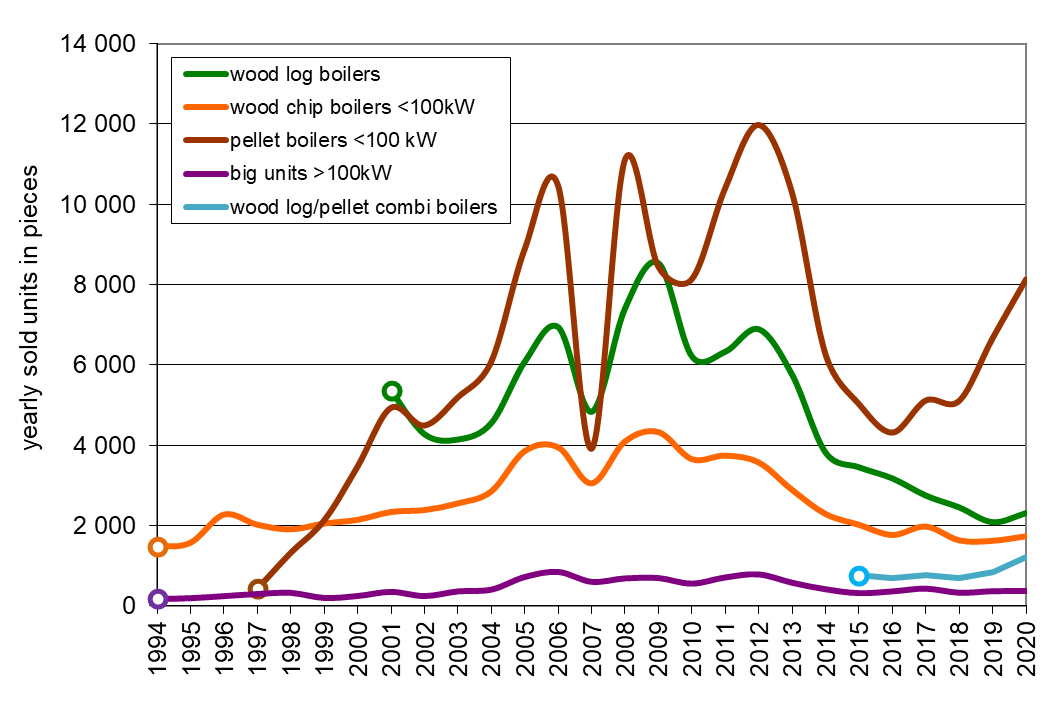

The market for biomass boilers steadily increased in Austria from 2000 until 2006 with a constantly high market growth. A market break of more than 40 % occurred 2007 for all types of biomass boilers due to low prices for heating oil and the mentioned supply shortage of pellets see Figure 8. The installation of additional pellet production capacities has eliminated the risk of shortage. In 2009 the sales figures declined again essentially by 24 % due to lower oil prices caused by the global finance and economic crisis. In the years 2011 and 2012 the sales of pellet boilers increased strongly facilitated by rather high heating oil prices and moderate pellet prices. In 2012 the market for pellet boilers was growing again with 15 % increase of sales. In 2013 the biomass boiler sales declined due to higher biofuel prices and the effect of investments in advance in the years after the economic crisis.

This trend also continued in the following years due to low oil prices and warm weather. In 2019 and 2020 the sale figures increased again. In 2020, the sales of pellet boilers (<100 kW) increased by 21.9 %, those of wood log/pellets combi by 45.2 %. The sales of small-scale (<100 kW) wood chip boilers increased by 6.9 % and the sales of wood log boilers by 10.9 %.

In 2020 8,132 pellet boilers, 2,315 wood log boilers, 1,215 wood log-pellet combi-boilers and 2,057 wood chip boilers were sold on the Austrian market, all boilers concerning the whole range of power. Furthermore at least 1,800 pellet stoves, 4,600 cooking stoves and 6,000 wood log stoves were sold. Austrian biomass boiler manufacturers typically export approximately 80 % of their production. The biomass boiler and stoves sector obtained a turnover of 1,016 million Euro in 2020. This resulted in a total number of 4,198 jobs in Austria. Currently and in next future research efforts are focused on the extension of the power range, further reduction of emissions and the use of biomass as an energy carrier in industrial and commercial processes with high heat demand. In addition to the technological quality, a further reduction of capital costs is decisive for achieving success in international markets.

Photovoltaic

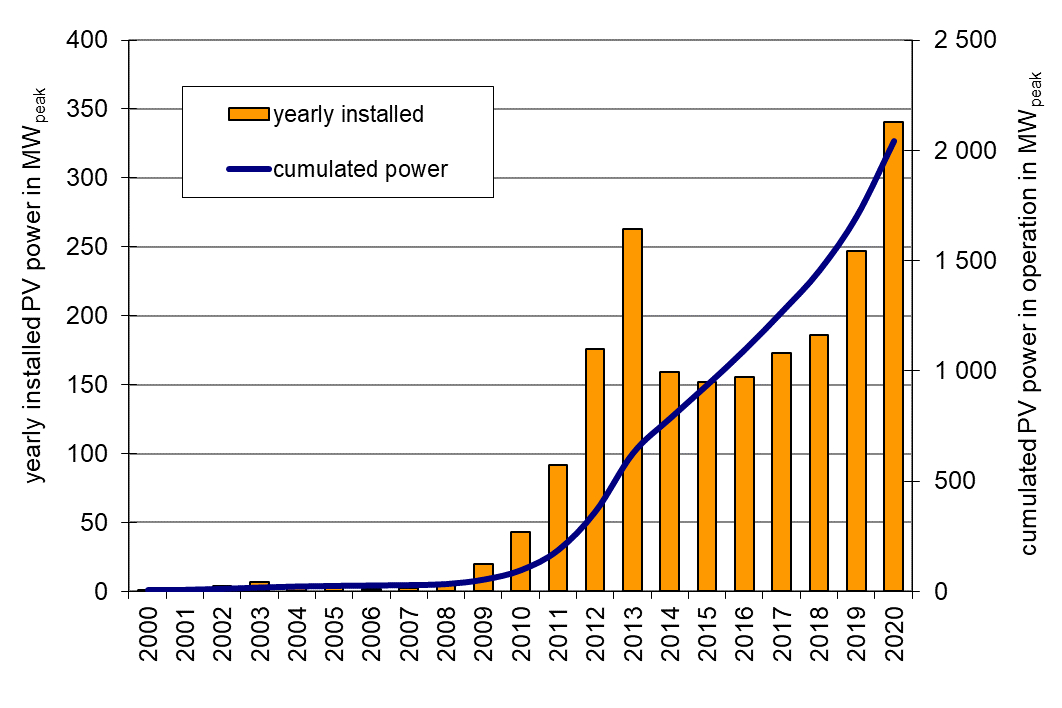

For the first time after the early phase of innovators and stand-alone systems the Austrian photovoltaic market in 2003 experienced an upsurge as the green electricity bill (Ökostromgesetz) was passed before collapsing again due to the 15 MWpeak capping of feed-in tariffs in 2004. After the absolute highest market diffusion of photovoltaic systems in Austria in 2013 due to an extra funding process, the PV market stabilized from 2014 to 2018. After an increase in 2019 to 247 MWpeak, also in 2020 a substantial increase was generated: As shown in Figure 9, PV plants with a total capacity of 340.84 MWpeak were installed in 2020, which represents a significant increase of 38 %.

Hence, in 2020 the total amount of installed PV capacity in Austria was 2,043 MWpeak. This represents an increase of 20 %. As a consequence, the sum of produced electricity by PV plants in operation amounted to at least 2,043 GWh in 2020 and lead to a reduction in CO2equ - emissions by 888,063 tons.

The Austrian photovoltaic industry is covering the production of PV modules and inverters as well as other PV components and devices. Furthermore, there is a high density of planning and installation companies for PV systems as well as specialized institutions and universities, which play an important role in international photovoltaic research & development (R&D). Within those economic sectors 2,755 persons are employed full-time, which raises solar technology to an overall substantial market. The average system price of a grid-connected 5 kWpeak photovoltaic system in Austria has decreased slightly compared to 2019 (1,568 EUR/kWpeak excl. VAT) to 1,506 EUR/kWpeak excl. VAT in 2020.

Especially the development of building integrated photovoltaic systems is of high importance for Austria. High added value seems to be achievable in this market branch. The integration does not only concern architectural aspects, but also systemic aspects of the optimal use of the locally generated electricity.

Solar thermal collectors

As early as the 1980s, the use of thermal solar energy experienced a first boom in the area of water heating and the heating of swimming pools. At the beginning of the 1990ies it was possible to develop a considerable market in the field of solar combi systems for hot water and space heating. In the period between the year 2002 and 2009 the solar thermal market grew significantly and reached the peak in 2009 due to rising oil prices but also due to new applications in the multifamily house sector, the tourism sector as well as new applications in solar assisted district heating and industrial process heat.

After the phase of massive growth until 2009, the domestic market has been declining for more than a decade. This development is not only observed in Austria, but with a few exceptions also in most European countries. In 2020, the Austrian domestic market again recorded a decline of 17.0 % compared to 2019.

As a positive aspect, it has to be emphasized that two large solar thermal plants for district heating systems with a total capacity of mit 4.6 MWth (6,543 m²) as well as a solar cooling system with a collector area of 3,500 m² and a cooling capacity of 660 kW were commissioned in 2020.

By the end of the year 2020 approx. 4.9 million m² of solar thermal collectors were in operation. This corresponds to an installed thermal capacity of 3.4 GWth. The solar yield of the solar thermal systems in operation is equal to 2,116 GWhth. The avoided CO2-emissions are 345,637 tons.

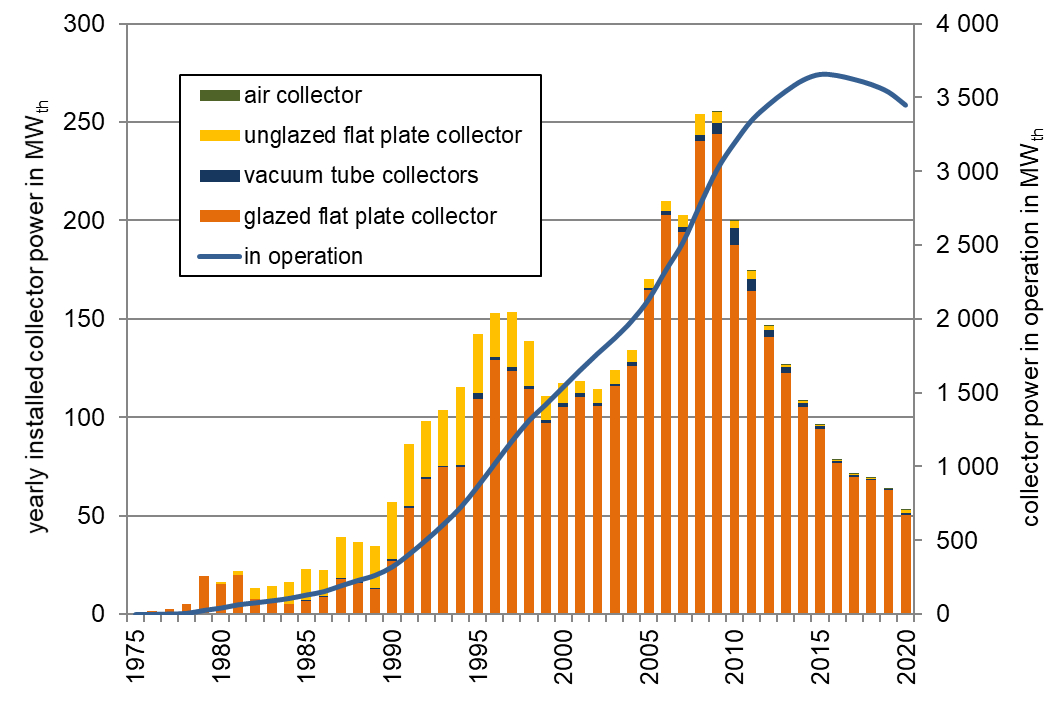

In 2020 a total of 76,060 m² solar thermal collectors were installed, which corresponds to an installed thermal capacity of 53.2 MWth as Figure 10 shows.

The export share of thermal collectors increased from 81 % in 2019 to 84 % in 2020. The turnover of the Austrian solar thermal industry was estimated with 131 million Euros for the year 2020. Therefore approx. 1,100 full time jobs can be numbered in the solar thermal business.

Heat pumps

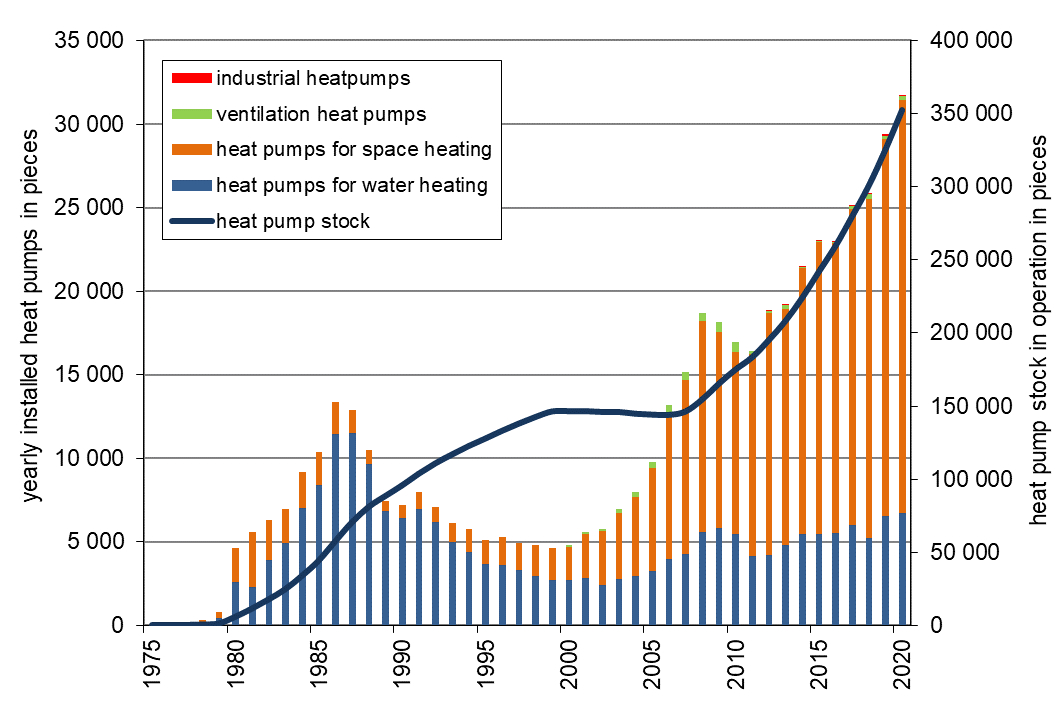

The historical development of the heat pump market shows an early phase of technology diffusion in the 1980's (mainly heat pumps for water heating), followed by a significant market decrease in the 1990's and a strong market diffusion starting from the year 2001 (now mainly heat pumps for space heating) see Figure 11. From 2001 onwards the diffusion of heat pumps for space heating came together with the introduction of energy efficient buildings with low heating energy demand which offered good conditions for an energy efficient and economically attractive operation of heat pumps. This is due to low temperature needs in heating systems and low energy consumption for space heating.

The total sales volume of heat pumps (domestic market plus export market for all uses and power classes) increased in 2020 from 43,665 units sold in the previous year to 47,192 units. This corresponds to a growth of 8.1 %. Growth was observed both in the domestic market (+8.0 %) and in the export market (+8.3 %). Strong growth was particularly noticeable for heat pumps for space heating up to 10 kW. Domestic hot water heat pumps showed an increase of 3.1 % in the home market and an increase of 1.7 % in the export market.

The percentage of the export market was 32.8 % in quantity of the total sales in 2020 and therefore roughly the same as in the previous year. In 2020 the Austrian heat pump sector (production, trade, installation and monetary value of heat) had an amount of total sales of 870 million Euro and 1,721 full time jobs. Thanks to the existing heat pump stock in Austria about 832.853 tons CO2equ of net emissions could be avoided in 2020.

Presently research and development of heat pump systems focus on innovative installations combined with other technologies: e.g. solar thermal systems or photovoltaic systems, new energy-services as air-conditioning, space cooling or applications in the context of renovating buildings in regard to humidity problems. The range of innovations is completed with the use of new driving energy as natural gas and the use of the heat pump technology in smart grids.

Wind power

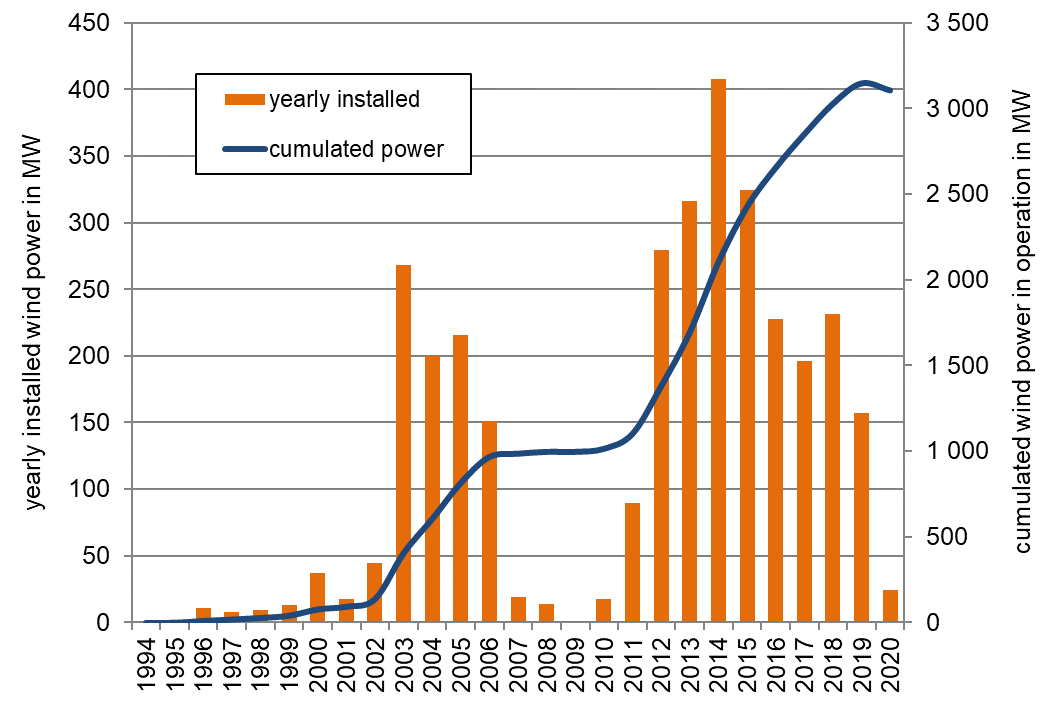

The historical market development of wind power in Austria is shown in Figure 12. While the expansion of wind power was able to continue at a low level in 2019, it almost completely came to a standstill in 2020. In Austria, only 7 new wind turbines with a total of 25 MW were built. Of the total of 7 plants, 4 plants with 17 MW were in Lower Austria, 3 plants with 8 MW in Burgenland. At the same time, around 66 MW of wind power capacity was decomissioned. This means that for the first time, the amount of wind energy extracted exceeds the added wind energy capacity. At the end of 2020, 1,295 wind turbines with a nominal output of 3,105 MW were connected to the grid. This capacity enabled an average annual electricity production of 7 TWh, which corresponds to approximately 11 % of the Austrian electricity consumption. Compared to the existing situation at the end of 2019, the electricity generation potential from wind power was even slightly reduced.

Approximately 981 million Euro turnover was generated by the windpower industry in Austria, including wind energy operators, suppliers and service companies. This means a slight increase compared to the previous year, mainly due to the proceeds from the electricity sales of the wind energy operators.

At the end of 2020, around 4,959 people were employed in the Austrian wind industry. Of these, 2,609 in the areas of construction, dismantling, maintenance and service and of these 481 for operators of wind turbines. Around 2,350 employees were reported from the supplying industry.

Thanks to the 2019 green electricity amendment, 250 projects with a capacity of 900 MW that have been approved and have been waiting to be implemented since 2015 can be equipped with subsidy contracts. As a result, more than 1 GW of wind power will be built by 2024 and investments of 1.6 billion Euros will be generated. In addition, 640 permanent jobs will be created.

Currently new projects have no prospect of a feed in tariff because the funds in the Green Electricity Act will be exhausted by the end of 2021. The industry is therefore waiting for the Renewable Energy Sources Act, which was announced for early 2021.

Conclusions

In 2020 the market development in the area of the investigated technologies in the Austrian domestic market was very heterogeneous – like in the previous years whereas the technology-specific trends of the past years have been most widely confirmed. Long-term stable developments are thereby merely the continuous growth of sales figures of heat pumps for space heating since the year 2000 and the on-going decrease of sales figures in the area of solar thermics which can be observed since the year 2010. A growth at least stretching over several years can be observed in the area of photovoltaics since the year 2017 and in the area of biomass boilers since 2019. In the year under review 2020 in the field of wind power only a slight expansion took place as was already the case in the period from 2007 to 2010 which led to a decrease of the active wind power output due to the concurrent decommissioning of old existing plants.

Concrete road maps for a decarbonisation of the Austrian energy supply in the areas electricity and heat are illustrated in the studies "Stromzukunft 2030" by Resch et al. (2016) and "Wärmezukunft 2050" by Kranzl et al. (2018). The diffusion rates of the technologies for the use of renewable energy necessary to achieve the national climate and energy targets are respectively clearly above the actually measurable developments.

Thus the annual electricity production from photovoltaics would have to be increased from 2.0 TWh in 2020 to 11.3 TWh in the year 2030 which corresponds to a continuing annual expansion of 930 MWpeak in the period from 2021 to 2030. The replacement of old plants does not play a significant role in the area of photovoltaics for this period because of the given diffusion trend. Consequently the expansion of photovoltaics in the year 2020 in the amount of 341 MW peak would already have to be increased by the factor 2.7 in the year 2021 for reaching the targets. If this increase does not happen immediately this failure has to be caught up on in the following diffusion process until 2030 – if the targets shall be reached. However, as a consequence this leads to constantly growing challenges.

In the area of wind power there would have to be an increase of the electricity production from 7.1 TWh in the year 2020 to 17.5 TWh in the year 2030. This corresponds to an annual net new installation of wind power plants in the range of approximately 456 MW for the period from 2020 to 2030 which also clearly surpasses the historical diffusion maximum of the year 2014 with 408 MW. Added to all this you have to consider that in the period from 2020 to 2030 round 1 GW wind power output is bound to be decommissioned and this output has to be compensated through additional new installations. This respectively applies provided that the expansion of further technologies for the supply of electricity on the basis of renewables like hydro power, biomass CHP, biogas and so on really takes place as presumed in the scenario and provided that the increase of the demand ranges within the assumed limits despite the electrification of the mobile sector.

Similar challenges have to be met in the heating area. In this area it is on the one hand the question of immediately preventing new installations of any kind of heat supply systems based on fossil energy including the further expansion of the thereby connected infrastructures and on the other hand it is the question of rapidly replacing the great stock of old installations for the use of fossil energy by renewables. The supposedly long, hereby available period of time until 2040 is tight even in the framework of ambitious scenarios due to the long life-cycles of installations and requires immediate action. Thus every in 2021 newly installed heating system on the basis of fossil energy will be part of the asset investment 2040 from a merely technical point of view and will prevent attaining the goals as these systems are usually in operation for more than 20 years. An early decommissioning of such systems in the further development is basically possible but it requires political courage (normative instruments) and the appropriate financial means (incentive oriented instruments and social cushioning).

A basic prerequisite for an entirely renewable heat supply is furthermore halving the energy consumption in the heat sector. Effective measures like the thermal renovation of buildings should happen synchronously to the switch to renewables. Buildings renovated with little ambition and their heat demand equally remain in the investment far past the targeted horizon 2040 and they consequently prevent reaching the goals in the heat area.

An important signal for the change in the heat sector was the termination of subsidies of new oil boilers by the Austrian Mineral oil industry in 2019 and the concurrent start of the "No more oil" campaigns at federal level and at the federal state level. This impulse has already led to clear growth effects of the pellets boilers and of the heat pumps. However the sales figures of heat supply systems on the basis of fossil energy show that the efforts so far to attain the goals have to be increased immediately and massively. The sale of natural gas condensing boilers was reduced by only 2 % to 46,000 pieces from 2019 to 2020 according to the association of Austrian suppliers of boilers and the sale of oil boilers was reduced by 35% to 3,000 pieces. Thus in 2020 still about 49,000 heat supply systems on the basis of fossil energy were newly installed in Austria. Almost every second heating system sold in Austria was therefore a system based on fossil energy.

The government programme 2020-2040 of the Austrian Federal Government contains a detailed, wide-ranging and ambitious programme for the topic climate protection and energy. It contains the clear goal of making Austria climate neutral until the year 2040. This plan brings along many chances for the Austrian economy which can make use of an advance in innovations and productions for market leaderships and patents. This approach also leads to the chance of a high national added value as an early expansion of the domestic market will also create great export opportunities. Austria could in this way regain its leading role in terms of climate protection and renewable energy and use it accordingly. As the technological and financial demand for the realisation of the government goal can be well estimated it is recommended to fix an appropriate obligatory plan up to the targeted horizon and to implement it in a manner which also mobilises investors and enables the necessary high diffusion rates.

Downloads

- Innovative Energy Technologies in Austria: Market Development 2020 (Full report only available in German) (pdf, 9.38 MB)

- Präsentationsunterlagen: Innovative Energietechnologien: Marktentwicklung 2020 (Peter Biermayr, ENFOS® e.U.), (Deutsch) (pdf, 1.12 MB)

- Presentation Slides: Innovative Energy Technologies in Austria, Market Development 2020 (Peter Biermayr, ENFOS® e.U.), (English) (pdf, 1.06 MB)