Innovative Energy Technologies in Austria: Market Development 2019

Bibliographic Data

14/2020P. Biermayr, C. Dißauer, M. Eberl, M. Enigl, H. Fechner, B. Fürnsinn, M. Jaksch-Fliegenschnee, K. Leonhartsberger, S. Moidl, E. Prem, C. Schmidl, C. Strasser, W. Weiss, M. Wittmann, P. Wonisch, E. Wopienka

Publisher: BMK

German, 266 pages

Content Description

Motivation, method and content

The documentation and market research in the field of technologies for the use of renewable energy sources creates a basis for the planning and decision making in politics, economy, research and development. The aim of this market study "Innovative energy technologies in Austria – market development 2019" is to lay a foundation in the following fields: biomass, photovoltaics, solar thermal collectors, heat pumps and wind power.

Methods used are: questionnaires handed out to manufacturers, trading firms and installation companies as well as questionnaires for funding providers at the national and local governments. Furthermore information is gathered with a survey of literature, the evaluation of available statistics and internet research. The obtained data is displayed in time series to provide the starting point for deeper analysis and strategical considerations.

First the market development is illustrated by production numbers or installed capacities and then the energy gain is calculated taking into account the life cycle of the machinery. The necessary support energy for the main and auxiliary machinery is discussed and savings in gross and net of greenhouse gas emissions are calculated. The graphically displayed turnovers and the job creating effects eventually show the impact of the various technologies in Austria. Results are shown in alphabetical order of technologies.

Introduction

In 2019 the market development of the technologies for the use of renewable energy was influenced by obstructing and promoting factors similarly to the previous years. The continually low to moderate prices of fossil energy sources, low rates of refurbishment, restrained signals from the area of energy-political instruments, the competition among technologies for the use of renewable energy itself and not least the mild weather conditions were diffusion-impeding. On the other hand the general economic growth and the increasing private expenses were diffusion-promoting. Against this background growth of the domestic market could only be observed in the areas of heat pumps, photovoltaics as well as wood pellets boilers in 2019. The sales of biomass fuels stagnated whereas the technological areas firewood boilers, biomass boilers, solarthermics and wind power partly had a clear decrease on the market.

Thus the trend of the reluctant to declining market development of the past years continues in 2019 even though winners and losers occasionally change over the years. Reliably and dynamically growing diffusion rates which would be necessary for a system change from fossil to renewable energy, could exclusively be observed in the sector heat pumps in the past years. If the national energy and climate goals which have been set for 2030 or 2040 should be reached the diffusion-impeding exogenous factors have to be confronted decisively. Therefore the efforts in the area of energy and environmental policy have to be clearly increased and the implementation of efficient instruments has to be strengthened.

Solid biomass - fuels

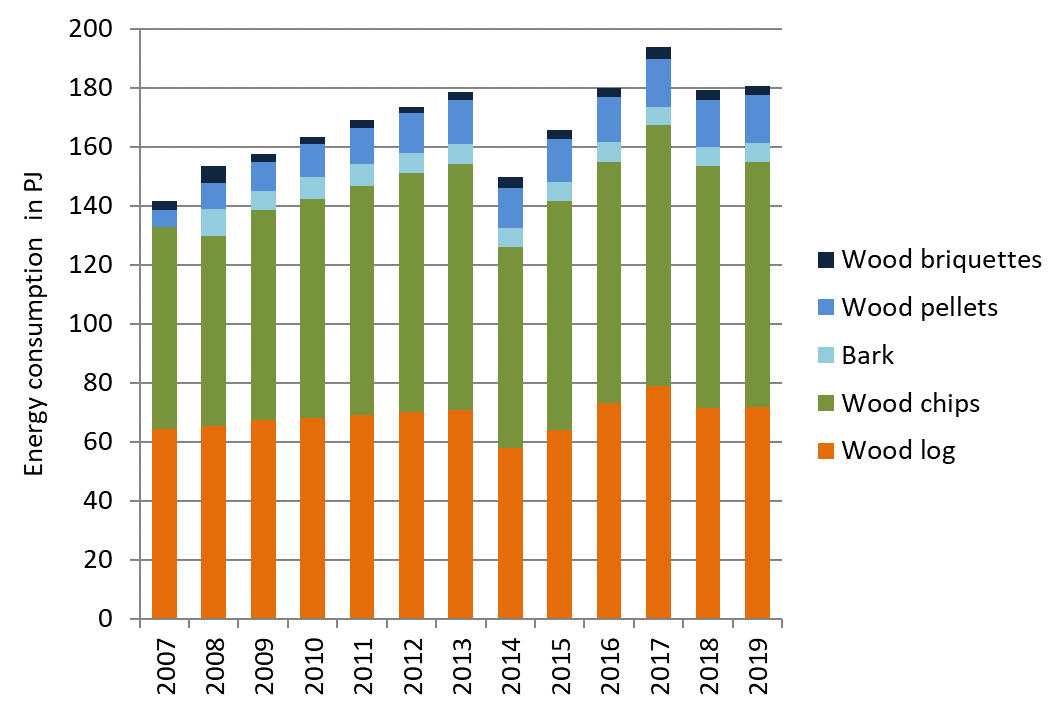

The energetic utilization of solid biomass has a long tradition in Austria and is still a very important factor within the renewable energy sector. The consumption of final energy from solid biofuels increased from 142 PJ in 2007 to 179 PJ in 2013. In 2014 the consumption of solid biofuels decreased to 150 PJ due to relatively high average temperatures see Figure 7. In the following years the consumption of solid biofuels increased again, in 2017 up to 193.6 PJ. However, due to high temperatures the consumption of solid biofuels decreased to 179.4 PJ in 2018 and to 180.5 PJ in 2019. The consumption of wood chips has been increasing since the beginning of the 1980s. In 2019 the wood chips consumption was 83.2 PJ and thus exceeded the consumption of wood logs with 71.7 PJ. The very well documented wood pellet market developed with an annual growth rate between 30 % and 40 % until 2006. This development was then stopped 2006 due to a supply shortage which resulted in a substantive price rise. The market recovered and the production capacity of 29 Austrian pellet manufacturers has been extended to 1.66 million tons a year. In 2019 the national pellet consumption amounts to 16.2 PJ (955,000 t).

Fuels from solid biomass contributed to a CO2 reduction of about 9.3 million tons in 2019. The whole sector of solid biofuels made a total turnover of 1.535 billion Euros thus creating 17,540 jobs.

The success of bioenergy highly depends on the availability of suitable biomasses in sufficient volumes and at competitive prices. The availability of biomass feedstock is currently very good. In addition to the traditional use of biomass in the heating sector, the importance of bioenergy as part of a sustainable energy system in combination with other renewables is increasing: biomass fuels are weather-independent energy suppliers. In this context the co-production of electricity and/or material products such as biochar is of great interest in order to ensure the most efficient use of resources.

Solid biomass – boilers and stoves

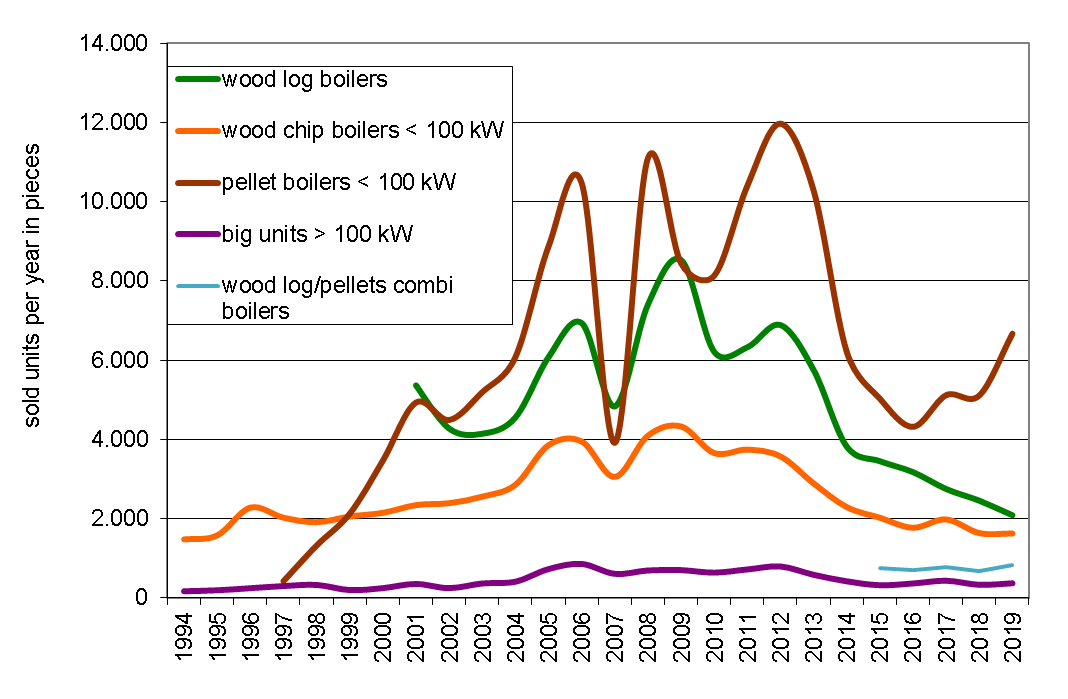

The market for biomass boilers steadily increased in Austria from 2000 until 2006 with a constantly high market growth. A market break of more than 40 % occurred 2007 for all types of biomass boilers due to low prices for heating oil and the mentioned supply shortage of pellets see Figure 8. The installation of additional pellet production capacities has eliminated the risk of shortage. In 2009 the sales figures declined again essentially by 24 % due to lower oil prices caused by the global finance and economic crisis. In the years 2011 and 2012 the sales of pellet boilers increased strongly facilitated by rather high heating oil prices and moderate pellet prices. In 2012 the market for pellet boilers was growing again with 15 % increase of sales. In 2013 the biomass boiler sales declined due to higher biofuel prices and the effect of investments in advance in the years after the economic crisis.

This trend also continued in the following years due to low oil prices and warm weather. In 2019 the sale figures increased, except for wood log boilers (-15.0 %). The sales of pellet boilers (<100 kW) increased by 30.5 %, those of wood log/pellets combi by 21.5 %. The sales of small-scale (<100 kW) wood chip boilers almost stagnate (-0.6 %)

In 2019 6,750 pellet boilers, 2,088 wood log boilers, 837 wood log-pellet combi-boilers and 1,920 wood chip boilers were sold on the Austrian market, all boilers concerning the whole range of power. Furthermore at least 1,838 pellet stoves, 5,494 cooking stoves and 6,368 wood log stoves were sold. Austrian biomass boiler manufactures typically export approximately 80 % of their production. The biomass boiler and stoves sector obtained a turnover of 942 million Euro in 2019. This resulted in a total number of 3,876 jobs in Austria. Research efforts are currently and in next future focused on the extension of the power range, further reduction of emissions and the use of biomass as an energy carrier in industrial and commercial processes with high heat demand. In addition to the technological quality, a further reduction of capital costs is decisive for achieving success in international markets.

Photovoltaic

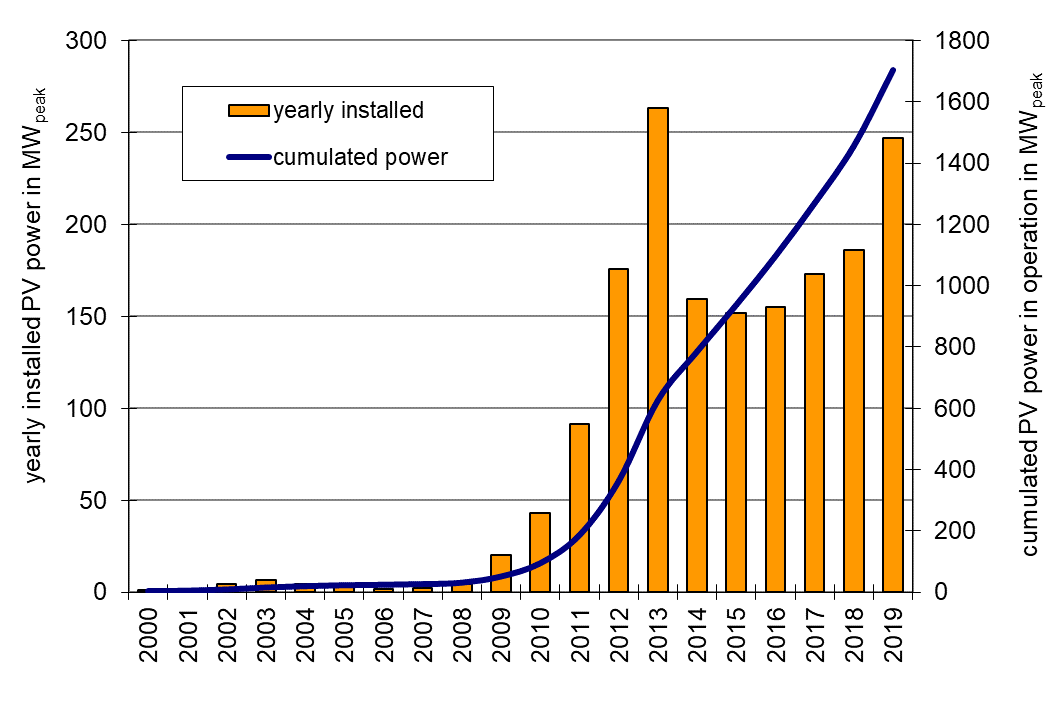

For the first time after the early phase of innovators and stand-alone systems the Austrian photovoltaic market in 2003 experienced an upsurge as the green electricity bill (Ökostromgesetz) was passed before collapsing again due to the capping of feed-in tariffs in 2004. After the absolute highest market diffusion of photovoltaic systems in Austria in 2013 due to an extra funding process, the PV market has stabilized from 2014 to 2018. However, in 2019 a substantial increase was generated: As shown in Figure 9, PV plants with a total capacity of 247.0 MWpeak were installed in 2019, which represents a significant increase of 32.7 %.

Hence, in 2019 the total amount of installed PV capacity in Austria was 1,702 MWpeak. This represents an increase of 17.0 %. As a consequence, the sum of produced electricity by PV plants in operation amounted to at least 1,702 GWh in 2019 and lead to a reduction in CO2 - emissions by 739,900 tons.

The Austrian photovoltaic industry is covering the production of PV modules and inverters as well as other PV components and devices. Furthermore, there is a high density of planning and installation companies for PV systems as well as specialized institutions and universities, which play an important role in international photovoltaic research & development (R&D). Within those economic sectors 2,749 persons are employed full-time, which raises solar technology to an overall substantial market. The average system price of a grid-connected 5 kWpeak photovoltaic plant (1,568 Euro/kWpeak) remained nearly unchanged in 2019.

Especially the development of building integrated photovoltaic systems is of high importance for Austria. High added value seems to be achievable in this market branch. The integration does not only concern architectural aspects, but also systemic aspects of the optimal use of the locally generated electricity.

Solar thermal collectors

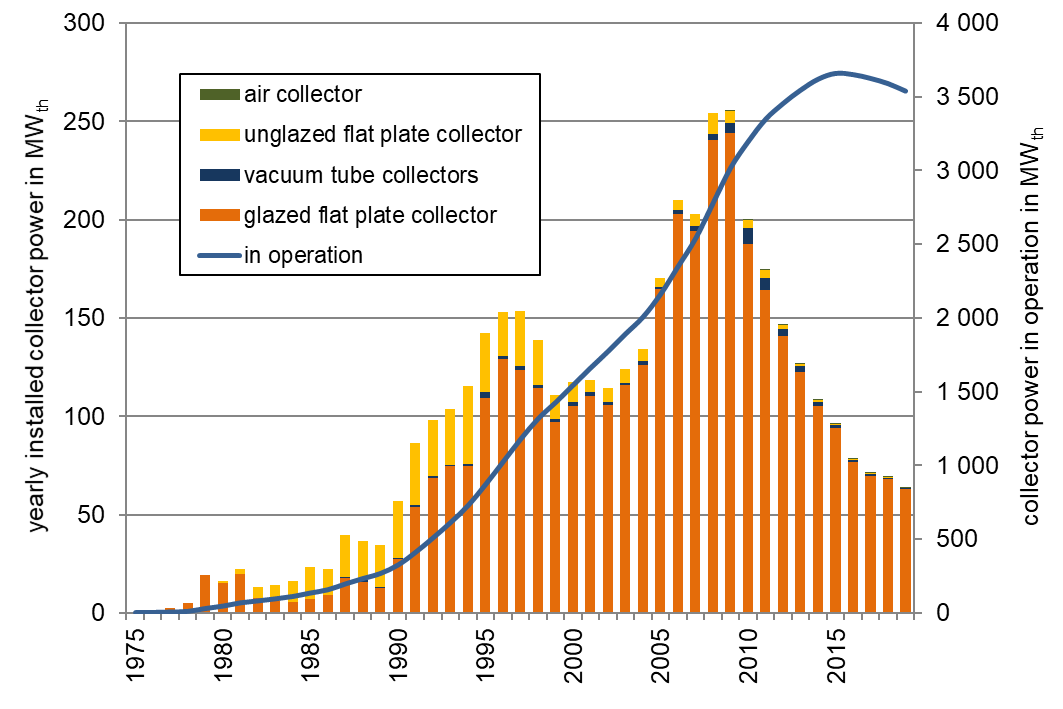

As early as the 1980s, the use of thermal solar energy experienced a first boom in the area of water heating and the heating of swimming pools. At the beginning of the 1990ies it was possible to develop a considerable market in the field of solar combi systems for hot water and space heating. In the period between the year 2002 and 2009. The solar thermal market grew significantly and reached the peak in 2009 due to rising oil prices but also due to new applications in the multifamily house sector, the tourism sector as well as new applications in solar assisted district heating and industrial process heat.

After the phase of massive growth until 2009, the domestic market has been declining for a decade. This development is not only observed in Austria, but with a few exceptions also in most European countries. In 2019, the Austrian domestic market again recorded a decline of 7.9 % compared to 2018.

By the end of the year 2019 approx. 5 million m² of solar thermal collectors were in operation. This corresponds to an installed thermal capacity of 3,5 GWth. The solar yield of the solar thermal systems in operation is equal to 2,081 GWhth. The avoided CO2-emissions are 353,713 tons.

In 2019 a total of 91.580 m² solar thermal collectors were installed, which corresponds to an installed thermal capacity of 64,1 MWth as Figure 10 shows.

The export rate of solar thermal collectors with 81 % in 2019 was on the same level as in 2018. The turnover of the Austrian solar thermal industry was estimated with 149 million Euros for the year 2018. Therefore approx. 1,200 full time jobs can be numbered in the solar thermal business.

Heat pumps

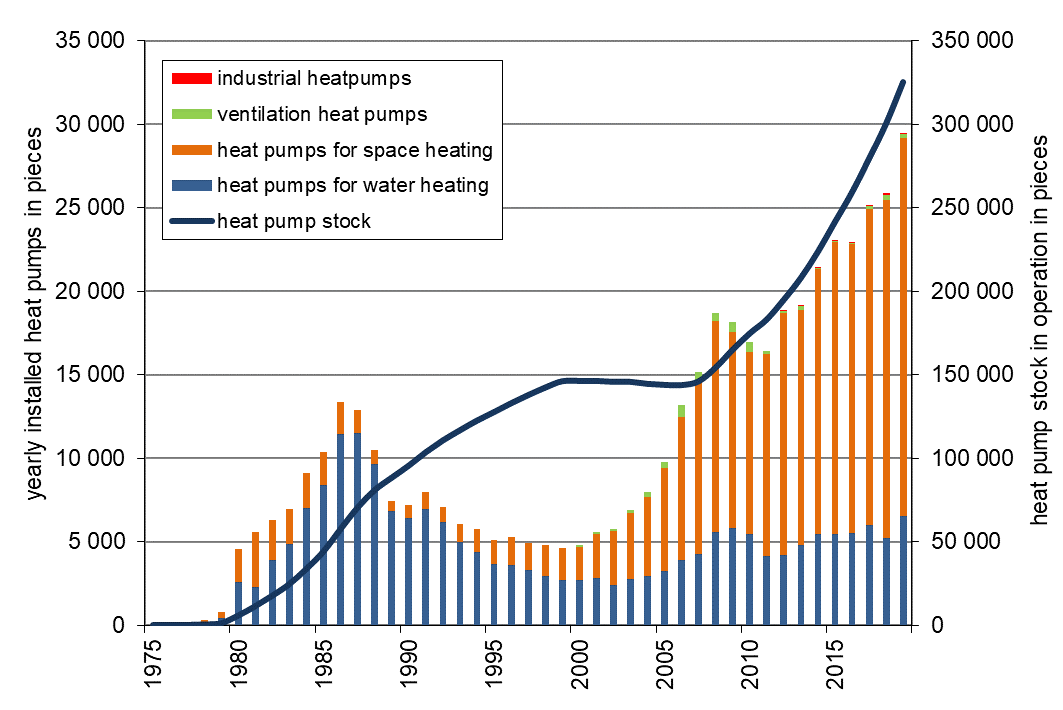

The historical development of the heat pump market shows an early phase of technology diffusion in the 1980's (mainly heat pumps for water heating), followed by a significant market decrease in the 1990's and a strong market diffusion starting from the year 2001 (now mainly heat pumps for space heating) see Figure 11. From 2001 onwards the diffusion of heat pumps for space heating came together with the introduction of energy efficient buildings with low heating energy demand which offered good conditions for an energy efficient and economically attractive operation of heat pumps. This is due to low temperature needs in heating systems and low energy consumption for space heating.

The total sales volume of heat pumps (domestic market plus export market) increased in 2019 from 34,604 units sold in the previous year to 39,138 units. This corresponds to a growth of 13.1 %. Growth was observed both in the domestic market (+13.9 %) and in the export market (+10.8 %). Strong growth was particularly noticeable in heat pumps for space heating up to 20 kW. Domestic hot water heat pumps showed an increase of 25.3 % in the home market and an increase of 8.4 % in the export market.

The percentage of the export market was 24.7 % in quantity of the total sales in 2019 and therefore slightly lower than in 2018. In 2019 the Austrian heat pump sector (production, trade, installation and monetary value of heat) had an amount of total sales of 796 million Euro and 1,551 full time jobs. Thanks to the existing heat pump stock in Austria about 778.561 tons CO2equ of net emissions could be avoided in 2019.

Presently research and development of heat pump systems focus on innovative installations combined with other technologies: e.g. solar thermal systems or photovoltaic systems, new energy-services as air-conditioning, space cooling or applications in the context of renovating buildings in regard to humidity problems. The range of innovations is completed with the use of new driving energy as natural gas and the use of the heat pump technology in smart grids.

Wind power

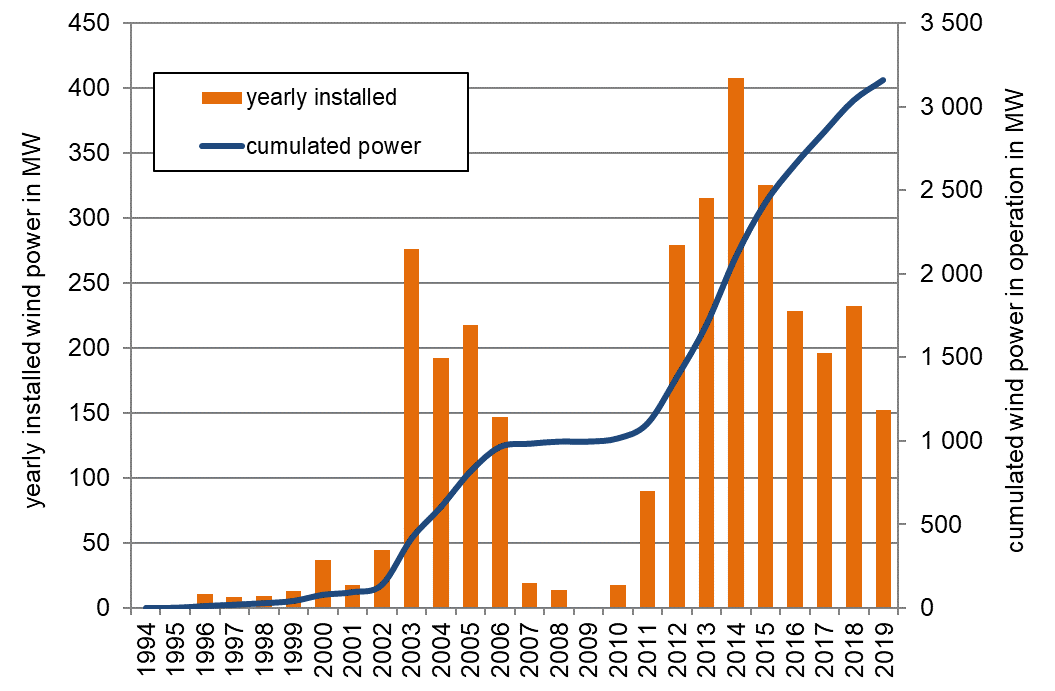

The historical market development of wind power in Austria is shown in Figure 12. Since 2018, for the first time in the history of Austrian wind power, the total installed capacity has been more than 3,000 MW. In 2019, the expansion of wind power continued at a low level. As a result, 49 new wind turbines with a total capacity of 152.4 MW were built in Austria. Of the total of 49 plants, 21 plants with 62.3 MW were built in Lower Austria, 8 plants with 23.8 MW in Styria and 20 plants with 66.3 MW in Burgenland. At the end of 2019, 1,340 wind turbines with a nominal output of 3,160 MW were on the grid. This output enabled an annual electricity production of 7.3 TWh, which corresponds to approximately 11 % of the Austrian electricity consumption. Compared to the portfolio at the end of 2018, the electricity generation potential from wind power increased by 7 %.

Approximately 1 billion Euro turnover was generated by the windpower industry in Austria, including wind energy operators, suppliers and service companies. This means a slight increase compared to the previous year, mainly due to the proceeds from the electricity sales of the wind energy operators. At the end of 2019, 3,555 people were employed in the Austrian wind power industry. Around 2,655 in the areas of construction, dismantling and maintenance, of which 470 working for operators of wind turbines. Around 900 employees were reported from the supplying industry.

Thanks to the 2019 green electricity amendment, 250 projects with a capacity of 900 MW that have been approved and have been waiting to be implemented since 2015 can be equipped with subsidy contracts. As a result, more than 1 GW of wind power will be built by 2024 and investments of 1.6 billion Euros will be generated. In addition, 640 permanent jobs will be created.

New projects currently have no prospect of a feed in tariff because the funds in the Green Electricity Act will be exhausted by the end of 2021. The industry is therefore waiting for the Renewable Energy Sources Act, which was announced for early 2021.

Conclusions

In 2019 – as in the year before the market development of the investigated technologies was very heterogeneous. Trends stable in the long-term were confirmed by continually decreasing sales figures of solar thermal collectors and continually increasing sales figures of heat pumps. The sale of biomass fuels stagnated while the sales figures of pellets boilers increased and the sales figures of firewood boilers decreased. The sales figures for photovoltaics increased and the new installations of wind power plants dropped to an 8 year low. In total there was a mix of developments beneficial and obstructive to the national climate and energy targets of 2030, 2040 or 2050 in 2019.

Concrete road maps for a decarbonisation of the Austrian energy supply in the areas electricity and heat are depicted in the studies "Stromzukunft 2030" by Resch et al. (2016) and "Wärmezukunft 2050" by Kranzl et al. (2018). The diffusion rates of technologies for the use of renewable energy, necessary for reaching the national climate and energy targets, are thereby each time clearly above the actually measurable developments.

Therefor the electricity production from photovoltaics of 1.7 TWh in 2019 would have to be increased to 11.3 TWh in 2030 which would correspond to a continuous annual growth of 873 Mwpeak in the period of 2020 to 2030. The growth of photovoltaics of 247 MWpeak in 2019 would therefor have to rise by a factor of 3.5 already in 2020. If this rise is not reached promptly the failure in the diffusion process has to be caught up on until 2030 – if the targets shall be reached which leads to ever-growing challenges. In the area of wind power there would have to be a rise of 7,3 Twh in 2019 to 17,5 Twh in 2030. This corresponds to annual new installations of wind power plants of net about 400 MW for the period of 2020 to 2030 which is equivalent to the historic diffusion maximum of 2014. This is valid under the presumption that in this scenario the supposed growth actually occurs equally for all other technologies of electricity supply on the basis of renewable energy like hydro power, biomass CHP, biogas etc. and that the increase of the need lies within the presumed limits.

Similar challenges have to be met in the heat area. In this area it is the point that new installations of heat supply systems on the basis of fossil energy are rapidly prevented and substituted by systems on the basis of renewable energy. On the other hand the great stock of installations for the use of fossil energy has to be quickly replaced by systems on the basis of renewable energy. The given period of time up to 2040 or 2050 seems to be long but is due to the long life cycle of installations even in the frame of ambitious scenarios relatively tight and demands immediate action. Here one has to further emphasize that a renewable heat supply can in any case only succeed if the energy consumption in the heat sector can be halved simultaneously thanks to an increase in efficiency which is taken by itself a great challenge.

In 2019 the market diffusion of the investigated technologies has been influenced by obstructing and favorable, endogenous and exogenous factors. Effective endogenous factors were the implemented energy political instruments, the efforts of companies and research institutions as well as the work of diffusion agents and lobbyists but also the competition among the technologies themselves. Exogenous influence came from the past mild winters, hot summers, the long-term low price of fossil energy and the slow cooling of the economy.

The beginning of the „Out of the oil" campaign can be seen as a favorable endogenous factor. A mixture of incentive-based, normative and informational instruments on various layers was hereby a strong signal for the economy and for the consumers. The message is definite and unmistakable and has already contributed without special focus on the normative components in 2019 to effects like the rise of sales figures of pellets boilers by 30.5 % and the rise of sales figures of heat pumps by 11.7 %. Finally in late 2019 the subsidies for new oil boilers by the Austrian oil economy was discontinued. Due to the funding pool within the period of obligation of the Kyoto protocol brought into being in 2009 in total more than 50,000 new oil boilers have been sponsored.

Considering the inactivity resulting from the existing power and fabric of interests on the one hand it is recommended to let the further market diffusion of oil boilers expire as soon as possible and to develop and establish a strategy aiming at „Out of natural gas" similar to the successful „Out of the oil" campaign. In many respects such a strategy is by far more complicated than the „Out of the oil" campaign as it is a massive impact on existing capital intensive infrastructures, company structures and great market shares. In this area lead-times will arise due to the necessary research and development activities which should be rapidly performed. Anyway in total it is technically and economically possible at least within 30 years (until 2050) to reduce the energy carrier natural gas to a minimum in the energy mix, see also Kranzl et al. (2018) and Resch et al. (2016).

The government program 2020-2024 of the Austrian Federal Government includes a detailed, extensive and ambitious program concerning the topics climate protection and energy. It includes the definite target to make Austria climate neutral until 2040. Thus the energy transition shall be executed quicklier than is planned for instance in the EU (2050). This courageous step bears many chances for the Austrian economy which could make use of an advance in innovations and productions for market leadership and patents. This approach further brings along the opportunity for a high national added value as an early expansion of the domestic market also creates high export opportunities. In this manner Austria could regain its leading role in terms of climate protection and renewable energy and use it accordingly. As technological and financial needs for the realization of the government target can be well estimated it is recommended to fix a mandatory corresponding plan for at least 10 years (2030) and thus implement it which mobilizes investors and makes the necessary diffusion rates possible.

The Corona crisis 2020 now questions all established systems and shows which measures are accepted and supported by humans in order to avert disaster from society. Now it is the question to present a future perspective for the economy and the society which makes confidence possible and offers new opportunities. The energy transition is such a program which can be realized with a fraction of the crisis-induced public extraordinary expenses and opens opportunities for generations.

Downloads