Innovative Energy Technologies in Austria - Market Development 2016

Bibliographic Data

13/2017Peter Biermayr, Christa Dißauer, Manuela Eberl, Monika Enigl, Hubert Fechner, Kurt Leonhartsberger, Florian Maringer, Stefan Moidl, Christoph Schmidl, Christoph Strasser, Werner Weiss, Patrik Wonisch, Elisabeth Wopienka

Publisher: BMVIT

German, 242 pages

Content Description

In 2016 the market development of the technologies using renewable energies was affected by repressive factors such as the continuously low prices for fuel and natural gas, the low rates of new buildings and renovations, the decreasing number of subsidies and not least the competition among the technologies themselves.

2016 these lasting constraints led to a further decrease of the sales figures in many sectors. Thus the sectors biomass boilers and stoves, solar thermal energy and wind power suffered from an important market decrease. In this background photovoltaics and heat pumps could at least maintain the sales figures of the year before. The sales in the sector of biomass fuels alone could be increased by 8.6 % due to weather conditions and the growth of biomass boilers stock.

The market figures of 2016 have to be seen as warning in regard to the national energy and climate targets for the year 2020 and beyond. Under the actual unfavourable conditions it is necessary to take effective and efficient measures without delay in order to reach this dynamic increase of the sales figures which then makes it possible to reach the intended targets.

Here in the short term and in the long term energy, environmental and research policy means have to be applied and combined with economical efforts to lead to new growth.

Solid biomass - fuels

The energetic utilisation of solid biomass has a long tradition in Austria and is still a very important factor within the renewable energy sector.

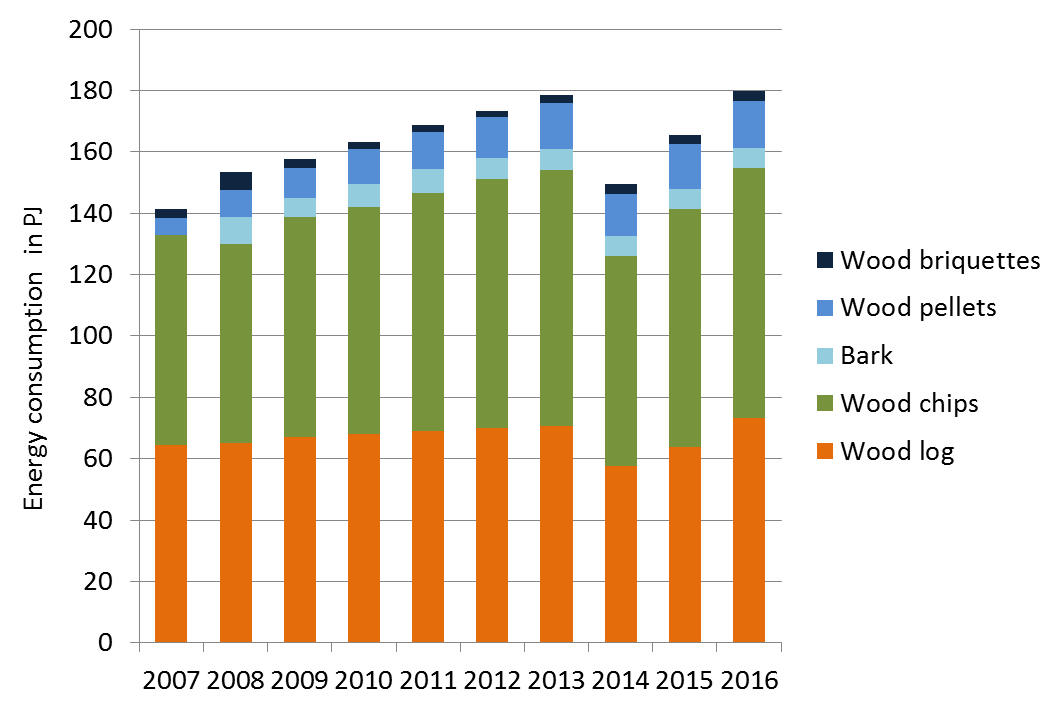

The consumption of final energy from solid biofuels increased from 142 PJ in 2007 to 179 PJ in 2013. In 2014 the consumption of solid biofuels decreased to 150 PJ due to relatively high average temperatures. In 2016, the consumption of solid biofuels increased again to 179.7 PJ. The consumption of wood chips has been increasing since the beginning of the 1980s.

In 2016 the wood chips consumption was 81.6 PJ and thus exceeds the consumption of wood logs with 69.2 PJ.

The very well documented wood pellet market developed with an annual growth rate between 30 and 40 % until 2006. This development was then stopped 2006 due to a supply shortage which resulted in a substantive price rise. But meanwhile the production capacity of 28 Austria pellet manufacturers has been extended to 1.45 million tons a year and this resulted in a market recovery.

In 2016 the national pellet consumption increased by 6 % compared to the previous year. The Austrian pellet production was around 15.3 PJ (900,000 t) in 2016.

Fuels from solid biomass contributed to a CO2 reduction of about 9.8 million tons in 2016. The whole sector of solid biofuels made a total turnover of 1,467 billion Euros thus creating 17,486 jobs.

The success of bioenergy highly depends on the availability of suitable biomasses in sufficient volumes and at competitive prices. Therefore, measures to mobilize additional energy wood potentials are needed. The upgrading of residues, co-products and waste from agriculture to solid biofuels will be important in the upcoming years since it is seen as high potential for the future extension of the biomass base.

The sustainable use of these biomass potentials requires the optimization of processes as well as technologies and the integration of cascading utilization paths as well as regional concepts. Furthermore, ecological boundaries should be considered. The establishment of sustainable supply and value chains and the cooperation of all actors along the value chain are of high importance.

Solid biomass – boilers and stoves

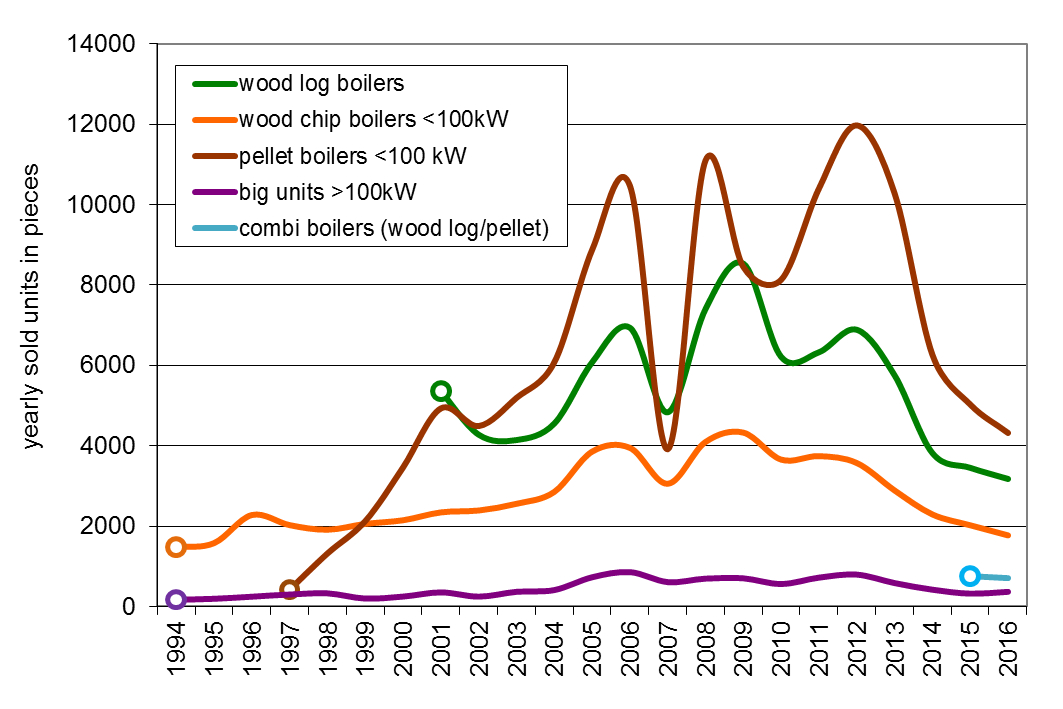

The market for biomass boilers has steadily increased in Austria from 2000 until 2006 with a constantly high market growth. A market break of more than 60 % occurred 2007 for all types of biomass boilers with low prices for heating oil and the mentioned supply shortage of pellets with significantly increased pellet prices. The installation of additional pellet production capacities has eliminated the risk of shortage.

In 2009 the sales figures declined again essentially by 24 % due to lower oil prices caused by the global finance and economic crisis. In the years 2011 and 2012 the sales of pellet boilers increased strongly facilitated by rather high heating oil prices and moderate pellet prices. In 2012 the market for pellet boilers was growing again with 15 % increase of sales which was the historical maximum so far.

In 2013 the biomass boiler sales declined due to higher biofuel prices and the effect of investments in advance in the years after the economic crisis. This trend also continued in 2014 and 2015 due to low oil prices and warm weather. 2016 a further decrease of the number of sales of all types of biomass boilers, except for big units > 100 kW, can be observed.

In 2016, the sales figures of pellet boilers decreased by 13.6 %, the sales of wood log boilers decreased by 8 % and the sale of small-scale (<100 kW) wood chip boilers decreased by 12.4 %.

In 2016 4,378 pellet boilers, 3,177 wood log boilers, 696 wood log-pellet combi-boilers and 2,083 wood chip boilers were sold on the Austrian market, all boilers concerning the whole range of power. Furthermore at least 1,773 pellet stoves, 5,468 cooking stoves and 8,638 wood log stoves were sold.

Austrian biomass boiler manufactures typically export approximately 80 % of their production. The biomass boiler and stoves sector obtained a turnover of 757 million Euro in 2016. This resulted in a total number of 3,162 jobs in Austria.

Research efforts are currently and in next future focused on the extension of the power range, further reduction of emissions with increased focus on the reduction of particulate matter (PM) emissions and the reduction of NOx emissions, on the development of specific new sensors for improved combustion control, optimisation of systems and combined systems (e.g. combined with solar thermal systems), annual efficiency improvement and on the development of market-ready small-scale and micro CHP systems.

Photovoltaic

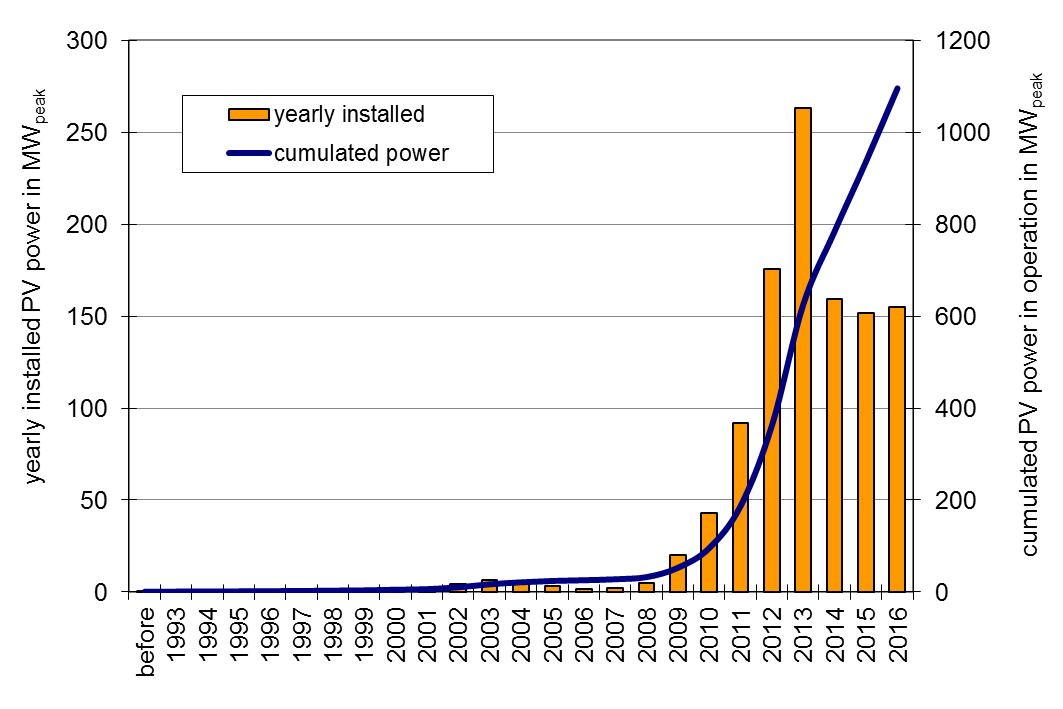

For the first time after the early phase of innovators and stand-alone systems the Austrian photovoltaic market in 2001 experienced an upsurge as the green electricity bill (Ökostromgesetz) was passed before collapsing again due to the capping of feed-in tariffs in 2004.

After the absolute highest market diffusion of photovoltaic systems in Austria in 2013, the PV market has stabilized from 2014 to 2016. As a result grid-connected plants with a total capacity of 154,802 kWpeak and stand-alone systems with a total capacity of approximately 952 kWpeak were installed in 2016.

Hence, in 2016 the total amount of installed PV capacity in Austria increased to 155,754 kWpeak, which led to a cumulated total, installed capacity of 1,096 MWpeak. As a consequence the sum of produced electricity by PV plants in operation amounted to 1,096 GWh in 2016 and lead to a reduction in CO2 - emissions by 920,653 tons.

The Austrian photovoltaic industry is highly diversified covering the production of PV modules and inverters as well as other PV components and devices.

Furthermore there is a high density of planning and installation companies for PV systems as well as specialized institutions and universities, which play an important role in international photovoltaic research & development (R&D). Within those economic sectors 2,822 persons are employed full-time which raises solar technology to an overall substantial market.

The average system price of a grid-connected 5 kWpeak photovoltaic plant in Austria decreased from 1,658 Euro/kWpeak in 2015 to 1,645 Euro/kWpeak in 2016, i.e. a reduction of 0.78 %.

Especially the development of building integrated photovoltaic elements is of high importance for Austria. High added value seems to be achievable in this market branch. Furthermore, due to the increased deployment of PV-systems, the question of PV grid integration becomes an important national driver for Smart Grids.

Solar thermal collectors

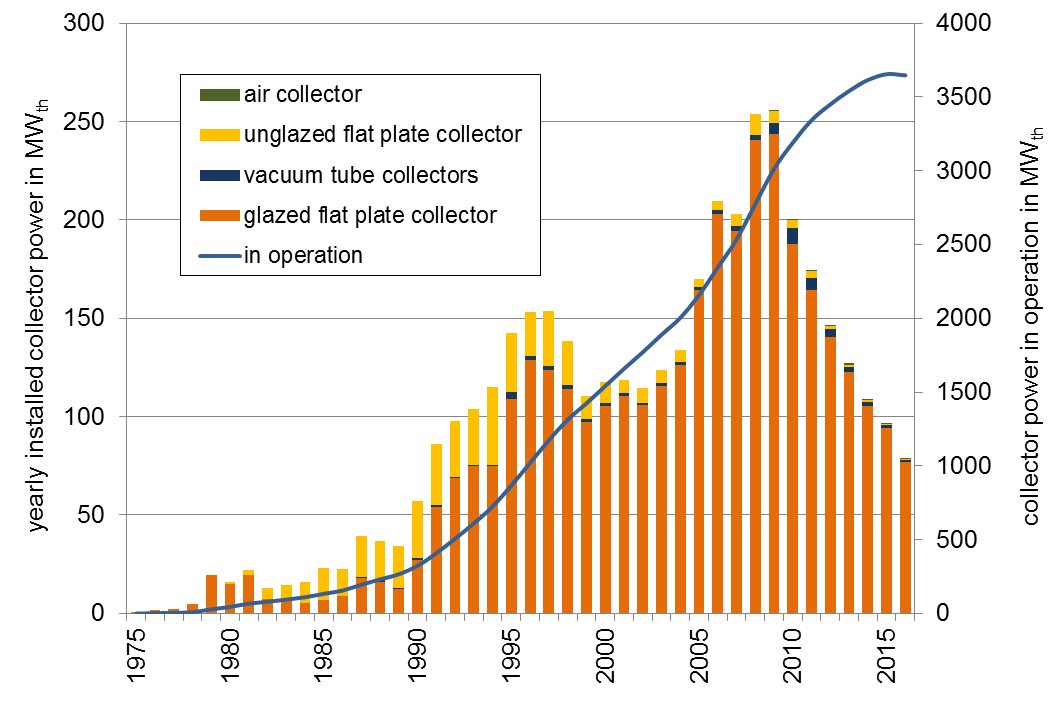

In Austria solar thermal systems for hot water preparation and swimming pool heating faced a first boom period already in the 1980ies. At the beginning of the 1990ies it was possible to develop a considerable market in the field of solar combi systems for hot water and space heating.

In the period between the year 2002 and 2009 the solar thermal market grew significantly and reached the peak in 2009 due to rising oil prices but also due to new applications in the multifamily house sector, the tourism sector as well as with new applications in solar assisted district heating and industrial process heat.

After this phase of massive growths the sector is facing a declining market in the seventh year in a row. In the beginning of this development this was caused by the effects of economic and financial crisis but is now mainly influenced by the growing competition with photovoltaic systems, the increased use of heat pumps as well as the still low prices of fossil fuels.

By the end of the year 2016 approx. 5.2 million m2 of solar thermal collectors were in operation. This corresponds to an installed thermal capacity of 3.6 GWth. The solar yield of the solar thermal systems in operation is equal to 2,130 GWhth. The avoided CO2-emissions are 426,473 tons.

In 2016 a total of 111,930 m2 solar thermal collectors were installed, which corresponds to an installed thermal capacity of 78.4 MWth. The development of the solar thermal collector market in Austria was characterized by a decrease of the sales figures of 19 % in 2016. The export rate of solar thermal collectors rose up to 83 %.

The turnover of the Austrian solar thermal industry was estimated with 196 million Euros for the year 2016. Therefore approx. 1,600 full time jobs can be numbered in the solar thermal business.

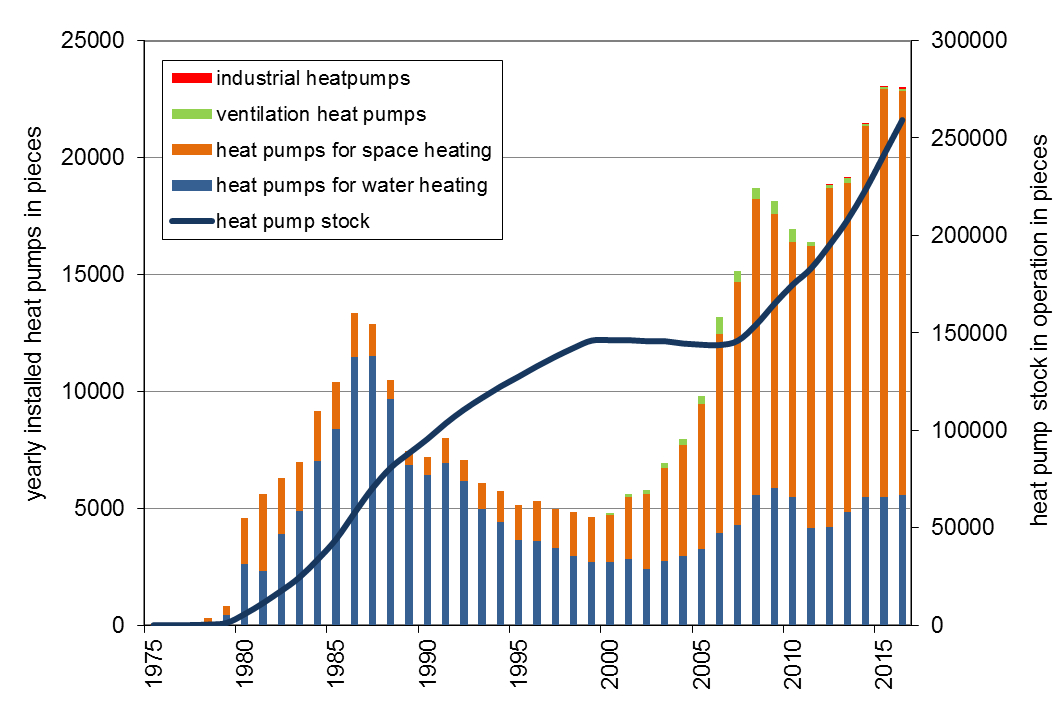

Heat pumps

The development of the Austrian heat pump market shows an early phase of technology diffusion in the 1980's (mainly heat pumps for water heating) followed by a significant market decrease and a second increase starting from the year 2001 (now mainly heat pumps for space heating).

The second diffusion period came together with the introduction of energy efficient buildings which offered good conditions for an energy efficient operation of heat pumps. This is due to the low temperature needs in the heating systems and low energy consumption for space heating.

The total sales of heat pumps (home market plus export market) decreased slightly from 2015 to 2016 by 0.4 %, from 33,141 plants to 33,017 plants. This is a stagnation on relatively high sales level. Slight decreases were observeable in both markets, domestic (-0.1 %) and export (-0.4 %).

In the domestic market heat pumps up to 50 kW power were affected by declines, while the sales figures for the power class with more than 50 kW doubled and heat pumps for water heating were able to record a growth of 1.3 %.

The percentage of the export market was 30.4 % in quantity of the total sales in 2016. In 2016 the Austrian heat pump sector (production, trade, installation and monetary value of heat) had an amount of total sales of 540 million Euro and 1,295 full time jobs. Thanks to the existing heat pump stock in Austria about 571,183 tons CO2equ of net emissions could be avoided in 2016.

Presently research and development of heat pump systems focus on innovative installations combined with other technologies: e.g. solar thermal systems for space and water heating or photovoltaic systems, new energy-services as air-conditioning, space cooling or applications in the context of renovating buildings in regard to humidity problems.

The range of innovations is completed with steady improvements of the technical energy efficiency, quality assurance measures, the use of new driving energy as natural gas and the use of the heat pump technology in smart grids.

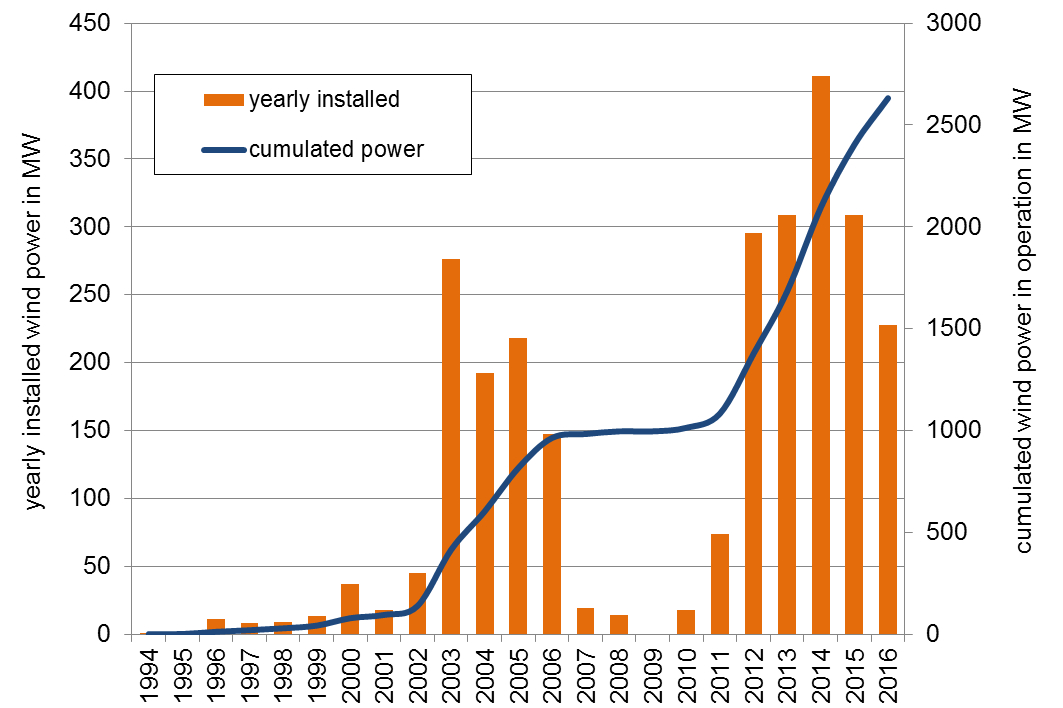

Wind power

Austrian wind power has developed in different periods. The first diffusion period was based on the "Ökostromgesetz 2001" and led to 1 GWel installed wind power. After some years with too low feed-in tariff the "Ökostromgesetz 2012" allowed to install new capacities starting with 2011 and led to a total capacity of 2.632 MWel by the end of 2016.

In 2016 75 turbines with a capacity of 228 MWel were installed. This is an increase in capacity of more than 10 % compared to 2015. The highest growth has been realized in Lower Austria (167,9 MWel), followed by Styria (42 MW), Burgenland (11,8 MW) and Upper Austria (6 MW).

In 2015 nearly 5,2 TWh electricity have been produced by wind turbines. The annual wind energy production saves more than 4,8 Million Tonnes CO2equ (under the assumption that imported fossile ENTSO-E mix has been substituted).

In terms of technology the newly installed turbines in 2016 were dominated by the 3 MWel class. 69 turbines of the 3 MWel class have been installed in 2016.

In 2016 Austrian turbine operators generated a turnover of more than 464 Mio. Euro. New installations of 228 MWel triggered investments of around 375 Mio. Euro and created a domestic added value of 105 Mio. Euro. The turnover of the Austrian wind industry reached nearly 529 Mio. Euro in 2016.

Based on the feedback of the questionnaires 1,739 persons were employed in the industry sector. 390 persons were employed by turbine operators. Considering the effects elaborated in the study „Wirtschaftsfaktor Windenergie", around 2,929 jobs come from turbine installation, operation and dismantling. In total the aggregated employment rate lies at 4,667 jobs (adjusted for duplications).

Downloads