Innovative Energy Technologies in Austria Market Development 2014

Content Description

Not only did the mild winter in 2013/14 reduce the hours of full load and the energy turnover of all heating boilers but statistically it also extended their lifespan. 2014 this had an effect on the entire boiler market which had a decline in sales of 8 %. Furthermore the oil price decline from September 2014 onwards caused many operators of oil boilers to refill their oil tank which had not been emptied. Thus the planned investment in the exchange of boilers was prevented.

The development of the Austrian economy was still restrained in 2014 especially in comparison with Germany. Furthermore the clearly rising unemployment caused in total a negative private and public investment environment. The tendency of the decreasing sales figures in the area of solar thermal energy continued in this environment. But even in the area of photovoltaics there was a clear decrease of new installations. The sale of heat pump systems stabilized on a relatively high level and only in the area of wind power there was a clear growth.

Solid biomass - fuels

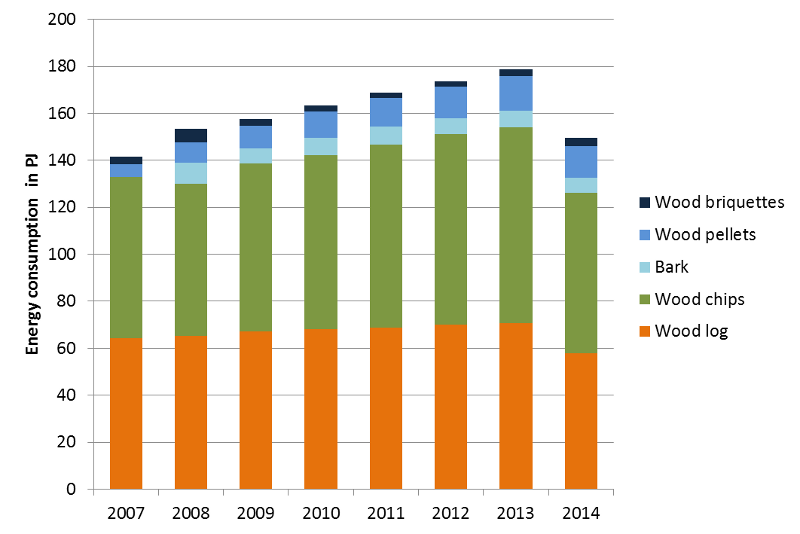

The energetic utilisation of solid biomass has a long tradition in Austria and is still a very important factor within the renewable energy sector. The consumption of final energy from sold biofuels increased from 142 PJ for 2007 to 179 PJ for 2013. In 2014, the consumption of solid biofuels decreased to 150 PJ due to relatively high average temperatures.

The consumption of wood chips has been increasing since the beginning of the 1980s. In 2013, the wood chips consumption was 83 PJ and thus exceeds the consumption of wood logs with 71 PJ. However, the wood chips consumption decreased to 68 PJ in 2014. The very well documented wood pellet market developed with an annual growth rate between 30 and 40 % until 2006. This development was then stopped 2006 due to a supply shortage which resulted in a substantive price rise.

But meanwhile the production capacity of 27 Austria pellet manufacturers has been extended to 1.48 million tons a year and this resulted in a market recovery. In 2014, due to the warm weather, the pellet consumption decreased by 7.4 % compared to the previous year. The pellet production in Austria was around 13.8 PJ (810,000 t) in 2014.

Fuels from solid biomass contribute to a CO2 reduction of almost 8.3 million tons for 2014. The whole sector of solid biofuels accounted a total turnover of 1,146 billion Euros and 10,234 jobs.

The success of bioenergy highly depends on the availability of suitable biomasses in sufficient volumes and at competitive prices.

Thereby short rotation forestry with willow and poplar planting is seen as highly potential for the future extension of the biomass base. In addition, the upgrading of residues, co-products and waste from agriculture to solid biofuels and the upgrading from other biogenic waste fractions to solid biofuels will be in the focus for the upcoming years. This development is determined by regulative policy measures such as the Common Agricultural Policy of the European Union. Furthermore, the development of bioenergy has to be coordinated with other biomass based branches and stakeholders. Together new synergies should be established to maximise added value from (especially regional) biomass.

Solid biomass - boilers and stoves

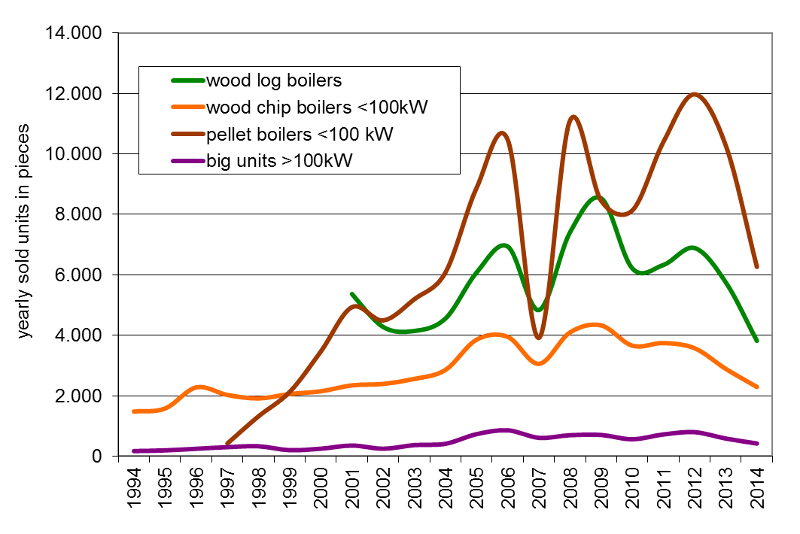

The market for biomass boilers has increased in Austria steadily from 2000 until 2006 with a constantly high market growth. A market break of more than 60 % occurred 2007 for all types of biomass boilers with low prices for heating oil and the mentioned supply shortage of pellets with significantly increased pellet prices. The installation of additional pellet production capacities has than eliminated the risk of shortage. In 2009 the sales figures declined again essential by 24 % due lower oil prices caused by the global finance and economic crisis. In the years 2011 and 2012 the sales of pellet boilers increased strongly facilitated by rather high heating oil prices and moderate pellet prices.

In 2012 the market for pellet boilers was growing again with 15 % increase of sales which was so far the historical maximum. In 2013 the biomass boiler sales declined due to higher biofuel prices and the effect of investments in advance in the years after the economic crisis. This trend also continued in 2014 due to low oil prices and warm weather. In 2014, the sales figures of pellet boilers decreased by even 39.5 %, the sales of wood log boilers decreased by 33.6 % and the sale of small-scale (

In 2014, on the Austrian market 6,266 pellet boilers, 3,820 wood log boilers and 2,658 wood chip boilers were sold, concerning the whole range of power. Furthermore, 2,399 pellet stoves, 6,710 cooking stoves and 11,692 wood log stoves were sold at least.

Austrian biomass boiler manufactures typically export approximately 75 % of their production. In Germany for instance two out of three installed biomass boilers are of Austrian origin. Germany and Italy are the biggest export markets for Austrian companies. The biomass boiler and stoves sector obtained a turnover of 828 million Euro in 2014. This resulted in a total number of 3,799 jobs in Austria.

Research efforts are currently and in next future focused on the extension of the power range, further reduction of emissions with increased focus on the reduction of particulate matter (PM) emissions and the reduction of NOx emissions, development of use specific new sensors for improved combustion control, optimisation of systems and combined systems (e.g. combined with solar thermal systems), annual efficiency improvement and in the development of market-ready small-scale and micro CHP systems.

Photovoltaic

For the first time after the early phase of innovators and stand-alone systems the Austrian photovoltaic market in 2001 experienced an upsurge as the green electricity bill (Ökostromgesetz) was passed before collapsing again due to the capping of feed-in tariffs in 2004. After the absolute highest market diffusion of photovoltaic (PV) systems in Austria in 2013, the PV market has stabilized in 2014. As a result grid-connected plants with a total capacity of 158,974 kWpeak and stand-alone systems with a total capacity of approximately 299 kWpeak were installed.

Hence, in 2014 the total amount of installed PV capacity in Austria increased to 159,273 kWpeak which led to a cumulated total installed capacity of 785.25 MWpeak. As a consequence the sum of produced electricity by PV plants in operation amounted to 785.25 GWh in 2014 and lead to a reduction in CO2 - emissions by 659,607 tons.

The Austrian photovoltaic industry is highly diversified covering production of PV modules and inverters as well as other PV components and devices. Furthermore there is a high density of planning and installation companies for PV systems as well as specialized institutions and universities, which play an important role in international photovoltaic research & development (R&D). Within those economic sectors a total of 3,213 persons are employed full-time which raises solar technology to an overall substantial and yet growing market.

The average system price of a grid-connected 5 kWpeak photovoltaic plant in Austria decreased from 1,934 Euro/kWpeak in 2013 to 1,752 Euro/kWpeak in 2014, i.e. a reduction of 9.39 %. This observation confirms a high economic learning rate, which is highly correlating to the still increasing world market. Especially the development of building integrated photovoltaic elements is of high importance for Austria. High added value seems to be achievable in this market branch. Furthermore, due to the increased deployment of PV-systems, the question of PV grid integration becomes an important national driver for Smart Grids.

Solar thermal collectors

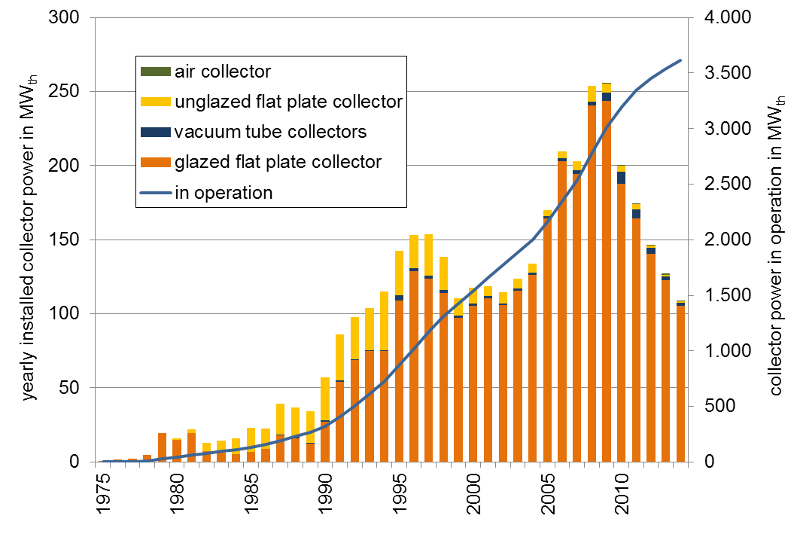

In Austria solar thermal systems for hot water preparation and swimming pool heating faced a first boom period already in the 1980ies. At the beginning of the 1990ies it was possible to develop a considerable market in the field of solar combi systems for hot water and space heating. In the period between the year 2002 and 2009 the solar thermal market grew significantly and reached the peak in 2009 due to rising oil prices but also due to new applications in the multifamily house sector, the tourism sector as well as with new applications in solar assisted district heating and industrial process heat. After this phase of massive growths the sector is facing a declining market in the fifth year in a row because of the effects of economic and financial crisis, low prices of fossil fuels and the growing competition with Photovoltaic systems.

By the end of the year 2014 approx. 5.2 million m2 of solar thermal collectors were in operation. This corresponds to an installed thermal capacity of 3.6 GWth. The solar yield of the solar thermal systems in operation is equal to 2.100 GWhth. The avoided CO2-emissions are 440,898 tons.

In 2014 a total of 155,170 m2 solar thermal collectors were installed, which corresponds to an installed thermal capacity of 108.6 MWth. The development of the solar thermal collector market in Austria was characterized by a decrease of the sales figures of 15 % in 2014. The export rate of solar thermal collectors was 82 % in 2014.

The turnover of the Austrian solar thermal industry was estimated with 255 million Euros for the year 2014. Therefore approx. 2,300 full time jobs can be numbered in the solar thermal business.

Heat pumps

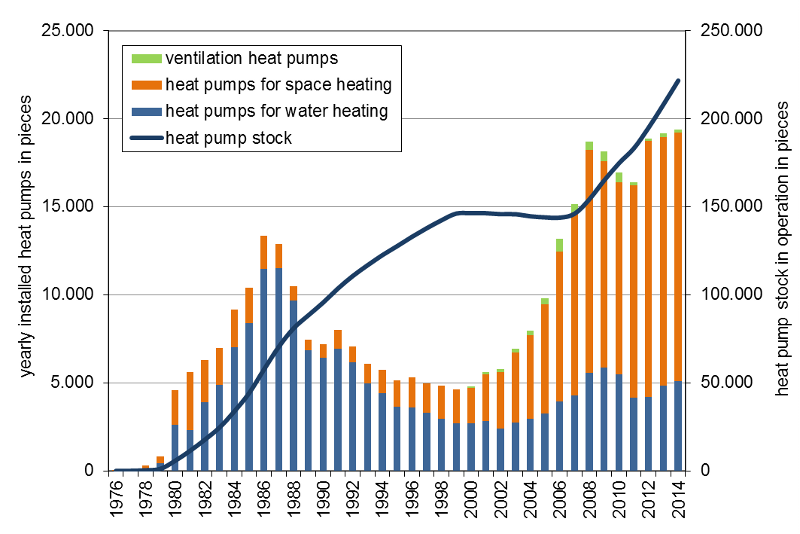

The development of the Austrian heat pump market shows an early phase of technology diffusion in the 1980's (mainly heat pumps for water heating) followed by a significant market decrease and a second increase starting from the year 2001 (now mainly heat pumps for space heating). The second diffusion period came together with the introduction of energy efficient buildings which offered good conditions for an energy efficient operation of heat pumps. This is due to the low temperature needs in the heating systems and low energy consumption for space heating.

The total sales of heat pumps (home market and export market) increased from 2013 to 2014 slightly by 1.0 %, from 28,959 plants to 29,236 plants which is a slight increase. Slight increases were observed in both the domestic market (+ 1.1 %) as well as the export market (+ 0.8 %). However, the growth in the domestic market was limited to the small capacity sector of up to 10 kW (+10.8 %) and the domestic hot water heat pumps (+5.2 %). All other power ranges and applications declined. In the export market slight gains could also be achieved in larger power segments.

The percentage of the export market was 33.7 % in quantity of the total sales in 2014. Therefore it was as high as in 2013. In 2014 the Austrian heat pump sector (production, trade and installation) had an amount of total sales of 245 million Euro and 1,246 full time jobs. In addition the monetary value of renewable energy provided was 198 million Euro.Thanks to the existing heat pumps in Austria about 504,290 tons CO2äqu of net emissions could be avoided in 2014.

Presently research and development of heat pump systems focus on innovative installations combined with other technologies: e.g. solar thermal systems for space and water heating or photovoltaic systems, new energy-services as air-conditioning, space cooling or applications in the context of renovating buildings in regard to humidity problems.

The range of innovations is completed with steady improvements of the technical energy efficiency, the use of new driving energy as natural gas and the use of the heat pump technology in smart grids.

Wind power

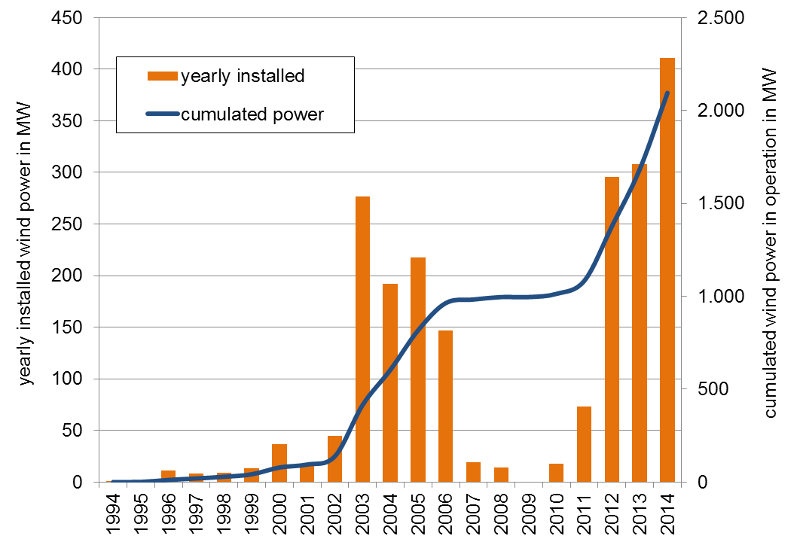

Austrian wind power has developed in different periods. The first diffusion period was based on the "Ökostromgesetz 2001" and led to 1 GWel installed wind power. After some years with too low feed-in tariff the "Ökostromgesetz 2012" allowed to install new capacities starting with 2011 and led to a total capacity of 2.095 MWel by the end of 2014.

In 2014 144 turbines with a capacity of 411 MWel were installed. This is an increase in capacity of more than 24 % compared to 2013. The highest growth rate has been realized in Burgenland (191 MWel), followed by Lower Austria (166 MWel), Upper Austria (15 MWel) and Styria (38 MWel). In 2014 nearly 3,9 TWh electricity have been produced by wind turbines. The annual wind energy production saves more than 3,3 Million Tonnes CO2equ (under the assumption that imported fossile ENTSO-E mix has been substituted).

In terms of technology 2014 was the first year in which the 3 MWel class dominated the newly installed turbines. More than 114 turbines of the 3 MWel class have been installed in 2014. In 2014 Austrian turbine operators earned nearly 300 Mio. Euro. New installations of 411 MWel triggered investments of around 678 Mio. Euro and created a domestic added value of 193 Mio. Euro. The turnover oft the Austrian wind industry reached more than 661 Mio. Euro in 2014. The majority (55 %) by the manufacturing industry. A high export orientation of the domestic wind industry is reflected by a export quota of 96 % in the manufacturing industry, followed by the infrastructure industry (39 %) and the service industry (33 %). The main export markets are Europe (64 %), Asia (21 %) and America (16 %).

Based on the feed back of the questionnaires 2,054 people have been employed in the industry sector. Furthermore 48 of 100 domestic turbine operators employed 383 people. Considering the effects elaborated in the study 'Wirtschaftsfaktor Windenergie" around 3,600 jobs come from turbine installation, operation and dismantling. In total the aggregated employment rate lies at 6,000 jobs (adjusted for duplications).

Kontakt

Technische Universität Wien, Energy Economics Group (EEG)

Dipl.-Ing. Dr. Peter Biermayr

Web: www.eeg.tuwien.ac.at

Bioenergy 2020+ GmbH

Dipl.-Ing. Christa Kristöfel, Dipl.-Ing. Dr. Monika Enigl,

Dipl.-Ing. Dr. Christoph Strasser, Dipl.-Ing. Dr. Christoph Schmidl, Dipl.-Ing. Dr. Elisabeth Wopienka

Web: www.bioenergy2020.eu

AEE INTEC

Dipl.-Päd. Ing. Werner Weiß, Manuela Eberl

Web: www.aee-intec.at

Technikum Wien GmbH

Kurt Leonhartsberger MSc., Dipl.-Ing. Hubert Fechner MAS MSc.

Web: www.technikum-wien.at

IG Windkraft

Mag. Stefan Moidl ,Florian Maringer

Web: www.igwindkraft.at